- GEICO is fully owned by Berkshire Hathaway, which acquired the company completely in 1996 after gradually increasing its ownership stake over several decades.

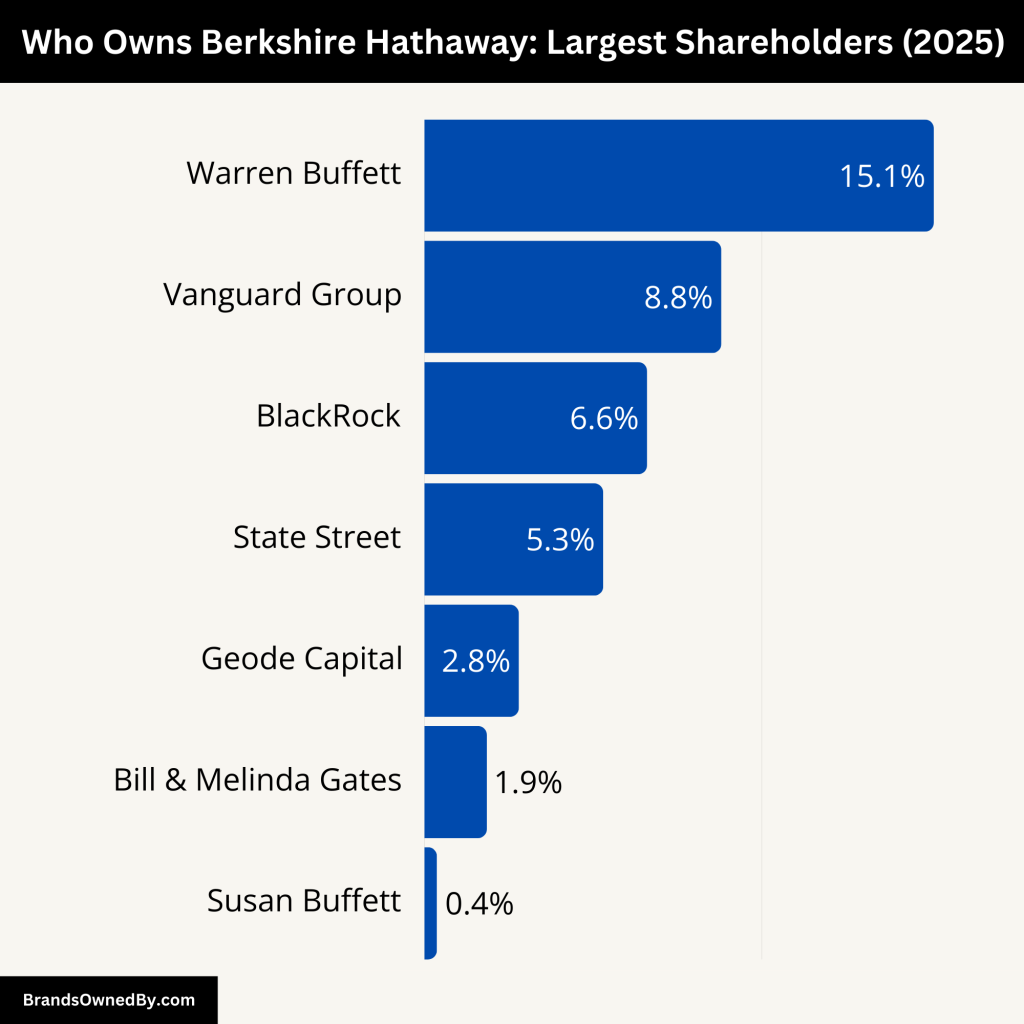

- Warren Buffett remains the most influential individual behind GEICO’s ownership structure because he is Berkshire Hathaway’s largest shareholder and played a major role in turning GEICO into one of the group’s most valuable insurance businesses.

- Since GEICO operates as a wholly owned subsidiary, it is not publicly traded. However, institutional investors including Vanguard Group, BlackRock, and State Street Corporation indirectly own stakes in GEICO through their shareholdings in Berkshire Hathaway.

- GEICO’s ownership under Berkshire Hathaway gives the insurer strong financial backing, long-term operational stability, and flexibility to invest heavily in advertising, underwriting systems, digital insurance platforms, and claims automation technology.

GEICO is one of the largest automobile insurance providers in the United States. The company built its reputation through affordable pricing, direct-to-consumer insurance sales, and large-scale advertising campaigns.

Unlike traditional insurers that depended heavily on local insurance agents, GEICO focused on selling policies directly to customers. This approach reduced operational costs and helped the company offer competitive premiums.

The company initially targeted government employees and military personnel. Over time, it expanded into the mainstream consumer market and became a nationally recognized insurance brand.

Today, GEICO offers a wide range of insurance products, including:

- Auto insurance

- Motorcycle insurance

- Commercial auto insurance

- RV insurance

- Renters insurance

- Homeowners insurance through partner networks.

The company is especially known for its digital-first strategy. Customers can purchase policies, manage claims, and access account services through mobile apps and online platforms.

Its marketing strategy also played a major role in brand growth. Campaigns featuring the GEICO Gecko became some of the most recognizable insurance advertisements in the United States.

GEICO competes directly with major insurance companies such as State Farm, Progressive Corporation, and Allstate.

GEICO Founders

GEICO was founded in 1936 by husband-and-wife business partners Leo Goodwin Sr. and Lillian Goodwin.

Leo Goodwin previously worked in the insurance industry and understood how risk selection affected profitability. He believed government employees represented lower-risk policyholders because they generally had stable employment and predictable driving behavior.

This insight became the foundation of GEICO’s business model.

Instead of trying to serve every customer segment immediately, the founders focused on a carefully selected market. That decision helped the company control claims risk during its early years.

Lillian Goodwin also played a major operational role in building the business. She helped manage administration and company operations while the company expanded.

The founders introduced a direct-sales insurance model that avoided heavy dependence on commissioned agents. This strategy later became one of GEICO’s biggest competitive advantages.

A practical example of this approach can still be seen today. Many traditional insurers maintain large physical branch networks, while GEICO continues to emphasize online services and centralized customer support systems.

Ownership History

The ownership history of GEICO is closely tied to its financial struggles, recovery strategy, and eventual acquisition by Berkshire Hathaway. The company evolved from a small specialized insurer into one of the most valuable insurance businesses in the United States.

Founding and Early Ownership Structure

GEICO was founded in 1936 by Leo Goodwin Sr. and Lillian Goodwin.

During its early years, the founders controlled the company privately. The business focused on providing auto insurance to federal employees and military personnel.

This narrow customer focus helped GEICO build a lower-risk insurance portfolio. The founders believed government workers were more financially stable and less likely to generate high insurance losses.

The company’s direct-sales model also reduced costs. Instead of relying heavily on insurance agents, GEICO sold policies directly to customers.

That approach helped the business expand rapidly during the mid-20th century.

Public Market Expansion

As GEICO grew, the company eventually became publicly traded.

Public ownership allowed GEICO to raise additional capital and expand operations across more states in the United States.

During this growth phase, the company moved beyond government employees and started targeting a broader consumer market.

The expansion increased policy sales significantly. However, it also exposed the company to greater underwriting risks.

Management pursued aggressive growth strategies during the late 1960s and early 1970s. In many cases, the company expanded faster than its risk controls could handle.

The Financial Crisis of the 1970s

GEICO faced a severe crisis during the 1970s.

The company experienced massive underwriting losses due to poor risk selection and rapid policy expansion. Claims costs increased sharply, while profitability declined.

At one point, many analysts believed GEICO could collapse financially.

The company lost a significant portion of its market value during this period. Thousands of policyholders and investors became concerned about the insurer’s future.

To survive, GEICO implemented major restructuring measures.

These changes included:

- Tightening underwriting standards

- Reducing high-risk policies

- Cutting operational costs

- Refocusing on profitable customer segments.

The restructuring helped stabilize the company over time.

Warren Buffett’s Early Investment in GEICO

The financial crisis attracted the attention of Warren Buffett.

Buffett already understood the company well. Earlier in his career, he had studied GEICO’s business model and believed the company had strong long-term potential.

During the 1970s crisis, Buffett saw an opportunity to invest in a struggling but fundamentally valuable insurance company.

Through Berkshire Hathaway, Buffett acquired a significant ownership stake in GEICO.

This investment became one of Berkshire Hathaway’s most successful long-term holdings.

Buffett admired GEICO’s low-cost structure and direct-sales model. He believed these advantages could help the company outperform competitors over time.

Berkshire Hathaway Increases Ownership

After GEICO recovered from its financial crisis, Berkshire Hathaway gradually increased its ownership position.

Over the following decades, Berkshire continued purchasing additional shares.

GEICO’s improving financial performance strengthened Berkshire’s confidence in the company.

The insurer expanded nationally and became one of the fastest-growing auto insurance companies in the United States.

Its heavy investment in advertising also increased brand recognition dramatically.

Commercial campaigns helped GEICO become a household name across America.

Full Acquisition by Berkshire Hathaway

In 1996, Berkshire Hathaway completed the full acquisition of GEICO.

The deal was valued at approximately $2.3 billion.

After the acquisition, GEICO became a wholly owned subsidiary of Berkshire Hathaway.

This meant GEICO no longer operated as an independent publicly traded company.

The acquisition gave GEICO access to Berkshire Hathaway’s financial strength and long-term investment philosophy.

Unlike many publicly traded companies that face pressure for short-term quarterly performance, GEICO gained more operational flexibility under Berkshire ownership.

Ownership Structure After the Acquisition

Since the acquisition, GEICO has remained fully owned by Berkshire Hathaway.

The company operates under Berkshire’s insurance division but maintains its own management and operational structure.

This arrangement allows GEICO executives to manage day-to-day operations while still benefiting from Berkshire Hathaway’s broader strategic oversight.

The ownership structure also supports long-term planning.

For example, GEICO has been able to invest heavily in technology systems, claims automation, and large-scale advertising campaigns without the same short-term shareholder pressure faced by some public competitors.

How Ownership Changed GEICO’s Strategy

Berkshire Hathaway ownership influenced GEICO’s strategic direction in several ways.

The company became more focused on disciplined underwriting and long-term profitability.

Management also invested heavily in operational efficiency.

GEICO continued expanding its direct-to-consumer model through digital platforms and online policy management systems.

This helped the company compete aggressively against traditional insurers with expensive agent networks.

A practical example of Berkshire’s influence can be seen during difficult insurance cycles. Instead of prioritizing rapid customer growth at any cost, GEICO often adjusted pricing and underwriting standards carefully to protect long-term margins.

That conservative strategy closely reflects Warren Buffett’s investment philosophy.

Who Owns GEICO?

![Who Owns GEICO [infographic]](https://brandsownedby.com/wp-content/uploads/2026/04/Who-Owns-GEICO-infographic-683x1024.png)

GEICO is fully owned by Berkshire Hathaway, the multinational holding company built around insurance, transportation, energy, manufacturing, and investment businesses.

GEICO operates as a wholly owned subsidiary under Berkshire Hathaway’s insurance division. This means Berkshire Hathaway owns 100% of the company and controls its long-term strategy, capital allocation, and corporate oversight.

The ownership structure is important because GEICO is not backed by private equity investors or short-term public shareholders focused on quarterly earnings pressure. Instead, it operates under Berkshire Hathaway’s long-term investment philosophy. That approach has shaped GEICO’s expansion strategy, underwriting discipline, pricing decisions, and technology investments for decades.

As of April 2026, Berkshire Hathaway remains one of the largest publicly traded companies in the world based on market value. The conglomerate controls a massive portfolio of businesses and investments, with insurance operations serving as one of its most important profit-generating segments.

GEICO plays a major role inside Berkshire Hathaway’s insurance ecosystem. The company generates billions of dollars in insurance premiums annually and contributes large amounts of insurance float that Berkshire can invest across its broader business empire.

Although GEICO itself is privately held under Berkshire Hathaway, ownership of Berkshire Hathaway is distributed among major shareholders including institutional investment firms, pension funds, and individual investors. The largest individual shareholder remains Warren Buffett, whose long-term investment strategy helped shape GEICO into one of America’s dominant auto insurers.

Parent Company: Berkshire Hathaway

Berkshire Hathaway is the direct parent company and sole owner of GEICO.

As of April 2026, Berkshire Hathaway controls a massive collection of businesses across multiple industries. Its portfolio includes insurance companies, railroads, energy utilities, manufacturing operations, retail businesses, and major stock investments.

The company owns businesses such as:

- BNSF Railway

- Berkshire Hathaway Energy

- Duracell

- Dairy Queen

- See’s Candies

- GEICO.

Insurance operations remain central to Berkshire Hathaway’s business model.

Beyond GEICO, Berkshire also controls major insurance businesses including:

- General Re

- National Indemnity Company

- Berkshire Hathaway Reinsurance Group.

These operations generate enormous insurance float that Berkshire uses for investments and acquisitions.

As of 2026, Berkshire Hathaway continues holding one of the largest corporate cash reserves in the world. This financial strength provides major stability for subsidiaries like GEICO during volatile insurance cycles.

The parent company’s decentralized management structure also affects GEICO operations.

Unlike many large corporations that centralize decision-making, Berkshire Hathaway typically allows subsidiaries to operate independently under their own management teams. GEICO executives handle daily insurance operations, pricing models, claims management, and customer acquisition strategies while still operating within Berkshire’s broader financial framework.

Another major advantage comes from Berkshire Hathaway’s long-term ownership approach.

Because Berkshire rarely sells core subsidiaries, GEICO operates with greater strategic stability than companies controlled by short-term investors or private equity firms. This allows the insurer to make large long-term investments in advertising technology, digital claims systems, and risk management infrastructure.

A practical example of Berkshire’s influence can be seen during difficult underwriting periods. Instead of aggressively pursuing risky policy growth to boost short-term revenue, GEICO has historically tightened underwriting standards and adjusted pricing discipline to protect long-term profitability.

That strategy closely reflects Berkshire Hathaway’s broader risk-management philosophy.

Acquisition of GEICO by Berkshire Hathaway

The relationship between GEICO and Berkshire Hathaway started long before the full acquisition.

Warren Buffett first became interested in GEICO in the 1950s when he studied the company’s direct-to-consumer insurance model. Buffett believed GEICO had a structural advantage because it avoided the high costs associated with traditional insurance agent networks.

During GEICO’s financial crisis in the 1970s, Berkshire Hathaway began investing heavily in the company.

At the time, GEICO faced severe underwriting losses caused by rapid expansion and poor risk management. Many investors believed the company could fail.

Buffett disagreed.

He believed GEICO’s core business model remained valuable despite its operational problems. Berkshire Hathaway purchased a significant ownership stake during the crisis period, helping establish a long-term relationship between the two companies.

Over the following decades, Berkshire gradually increased its ownership position.

In 1996, Berkshire Hathaway completed the full acquisition of GEICO in a deal valued at approximately $2.3 billion.

The acquisition allowed Berkshire Hathaway to fully integrate GEICO into its insurance operations.

After becoming a wholly owned subsidiary, GEICO expanded aggressively across the United States. The company increased advertising spending significantly and invested heavily in digital insurance infrastructure.

The acquisition also strengthened Berkshire Hathaway’s insurance float strategy. Insurance float refers to premium money collected before claims are paid. Berkshire uses this capital across investments and acquisitions throughout its broader business portfolio.

GEICO eventually became one of Berkshire Hathaway’s most strategically important subsidiaries.

Competitor Ownership Comparison

The ownership structure of GEICO is very different from many of its largest competitors in the insurance industry. Some insurers are publicly traded corporations. Others operate as mutual companies owned by policyholders.

These ownership models influence how each company approaches pricing, expansion, profitability, customer service, and long-term strategy.

GEICO’s ownership under Berkshire Hathaway gives it strong financial backing and long-term operational flexibility. Competitors often operate under different financial pressures depending on who owns them.

| Insurance Company | Ownership Structure | Parent Owner or Shareholders | Business Model Impact | Key Competitive Difference |

|---|---|---|---|---|

| GEICO | Wholly owned subsidiary | Berkshire Hathaway owns 100% of GEICO | Strong financial backing and long-term operational flexibility | Heavy focus on direct-to-consumer sales, digital insurance systems, and disciplined underwriting |

| State Farm | Mutual company | Owned by policyholders | Profits can be reinvested into customer services and policyholder benefits | Large agent network and strong customer retention strategy |

| Progressive Corporation | Publicly traded company | Owned by institutional and retail shareholders | Strong pressure for quarterly financial performance and growth | Advanced pricing analytics and strong telematics programs |

| Allstate | Publicly traded company | Owned by public shareholders and institutional investors | Focus on shareholder returns, profitability, and dividends | Combines agent-based sales with growing digital insurance operations |

| USAA | Member-owned organization | Owned by eligible members and policyholders | Focus on serving military members and long-term customer satisfaction | Specialized financial and insurance products for military families |

| Liberty Mutual | Mutual insurance company | Owned by policyholders | Greater focus on policyholder value over stock market performance | Broad insurance product portfolio with global operations. |

GEICO Ownership Structure

GEICO operates as a wholly owned subsidiary of Berkshire Hathaway.

This structure gives the company access to one of the strongest corporate balance sheets in the world.

Because Berkshire Hathaway follows a long-term investment philosophy, GEICO can focus heavily on underwriting discipline, operational efficiency, and long-term profitability instead of short-term quarterly growth targets.

Another advantage is financial stability during difficult insurance cycles.

For example, when accident claims, repair costs, or litigation expenses rise sharply, GEICO can rely on Berkshire Hathaway’s financial strength to absorb volatility more effectively than many smaller insurers.

The company also benefits from access to capital for technology upgrades, advertising expansion, and digital infrastructure investments.

State Farm Ownership Model

State Farm operates under a mutual ownership structure.

This means the company is technically owned by its policyholders rather than public shareholders.

Under this model, profits can be reinvested into the business or used to improve policyholder benefits, pricing strategies, and claims services.

Because there are no outside shareholders demanding stock price growth, State Farm can sometimes prioritize customer retention and long-term policyholder relationships over aggressive profit expansion.

State Farm also operates through a massive agent-based distribution network.

Unlike GEICO’s direct-sales approach, State Farm depends heavily on local insurance agents who manage customer relationships and policy sales.

This creates higher operating costs but can improve customer interaction and local service availability.

Progressive Ownership Structure

Progressive Corporation is a publicly traded company.

Its shares are owned by institutional investors, mutual funds, hedge funds, and retail shareholders.

Because Progressive is publicly traded, management faces strong pressure to deliver consistent quarterly financial performance.

The company focuses heavily on analytics-driven underwriting and pricing models.

Progressive became known for using advanced telematics and usage-based insurance programs earlier than many competitors.

Like GEICO, Progressive also emphasizes direct-to-consumer insurance sales. However, it still works with independent insurance agents alongside its direct business channels.

A practical difference between Progressive and GEICO can be seen in investor expectations.

Public shareholders often expect strong quarterly earnings growth from Progressive. GEICO, under Berkshire Hathaway ownership, typically operates with more flexibility to prioritize long-term insurance performance.

Allstate Ownership Structure

Allstate is also a publicly traded insurance company.

The company is owned by public shareholders and institutional investors.

Allstate historically relied heavily on exclusive insurance agents, although it later expanded digital insurance capabilities to compete more aggressively with companies like GEICO and Progressive.

Because Allstate operates under public market expectations, management often balances profitability goals with shareholder return expectations, including dividends and stock buyback programs.

GEICO’s structure differs because Berkshire Hathaway generally reinvests capital strategically across its businesses rather than focusing primarily on quarterly shareholder payout expectations.

USAA Ownership Structure

USAA operates under a member-owned structure.

The company primarily serves military members, veterans, and their families.

Its ownership model is somewhat similar to mutual insurance organizations because members benefit from the company’s financial performance.

USAA built a strong reputation for customer satisfaction and specialized military-focused financial services.

Unlike GEICO, USAA restricts eligibility requirements for membership and insurance access.

GEICO originally focused on government employees and military personnel, but later expanded broadly into the general consumer market.

Liberty Mutual Ownership Structure

Liberty Mutual operates as a mutual insurance company.

Like State Farm, the company is owned by policyholders rather than public shareholders.

This structure allows Liberty Mutual to focus more heavily on long-term policyholder value instead of stock market performance.

However, mutual ownership can sometimes limit access to external capital compared to publicly traded competitors.

GEICO benefits from Berkshire Hathaway’s enormous financial resources without needing to issue public shares independently.

How Ownership Structures Impact Competition

Ownership structures directly influence how insurance companies compete in the market.

GEICO’s Berkshire Hathaway ownership creates several strategic advantages:

Long-Term Strategic Flexibility

GEICO can make long-term operational decisions without excessive pressure from short-term public market expectations.

For example, the company may temporarily reduce customer acquisition growth if underwriting conditions become too risky.

Capital Strength

Berkshire Hathaway’s financial backing gives GEICO strong capital support during difficult market conditions.

This became especially important during periods of rising repair costs, inflation-driven claims increases, and severe weather-related insurance losses.

Technology Investment Capacity

GEICO has invested heavily in digital insurance infrastructure, mobile claims systems, and online customer management tools.

Berkshire Hathaway’s financial resources help support these long-term investments.

Advertising Power

GEICO became one of the most heavily advertised insurance brands in America.

The company’s massive advertising budgets helped build national brand recognition through campaigns like the GEICO Gecko and sports sponsorships.

Berkshire Hathaway’s ownership stability allowed GEICO to sustain long-term advertising investments consistently over many years.

Risk Management Philosophy

GEICO’s ownership under Berkshire Hathaway also influences its risk culture.

The company generally focuses heavily on disciplined underwriting and controlled expansion strategies.

This conservative approach reflects Warren Buffett’s long-standing emphasis on risk management and sustainable profitability.

A practical example can be seen during challenging insurance environments. Instead of aggressively cutting prices to chase market share, GEICO has historically adjusted pricing models carefully to maintain underwriting profitability over the long term.

Who Controls GEICO?

Although GEICO is fully owned by Berkshire Hathaway, the company operates through a layered leadership and management structure.

Control of GEICO is divided between Berkshire Hathaway’s long-term corporate oversight and GEICO’s executive leadership team that manages daily operations.

This structure allows GEICO to operate independently while still aligning with Berkshire Hathaway’s broader financial and risk-management philosophy.

Berkshire Hathaway’s Control Over GEICO

As the sole owner of GEICO, Berkshire Hathaway holds ultimate control over the company.

The parent company has authority over:

- Major strategic direction

- Executive leadership decisions

- Capital allocation

- Financial oversight

- Long-term operational priorities.

However, Berkshire Hathaway is known for its decentralized management model.

Unlike many conglomerates that tightly control subsidiaries, Berkshire usually allows its businesses to operate independently under their own executive teams.

This means GEICO leadership manages most day-to-day insurance operations without constant direct intervention from Berkshire headquarters.

Still, major corporate decisions and long-term strategic shifts remain influenced by Berkshire Hathaway leadership.

Warren Buffett’s Historical Influence

Warren Buffett played a major role in shaping GEICO’s long-term direction.

Buffett admired GEICO’s direct-sales insurance model for decades. He believed the company had structural advantages because it avoided many of the costs associated with traditional insurance agent networks.

His investment philosophy strongly influenced GEICO’s operating culture.

Under Buffett’s influence, GEICO focused heavily on:

- Underwriting discipline

- Long-term profitability

- Conservative risk management

- Operational efficiency

- Scalable advertising strategies.

A practical example of this philosophy appeared during difficult insurance cycles. Instead of aggressively pursuing risky policy growth, GEICO often tightened underwriting standards and adjusted pricing strategies to protect long-term margins.

That conservative approach closely reflected Buffett’s broader investment principles.

Todd Combs and Operational Leadership

Todd Combs became one of the most important executives overseeing GEICO’s operations in recent years.

Combs also holds senior leadership responsibilities within Berkshire Hathaway.

His involvement increased significantly as GEICO faced rising claims costs, underwriting pressure, and operational restructuring challenges.

Under his leadership influence, GEICO focused on improving:

- Claims efficiency

- Underwriting performance

- Technology modernization

- Cost management

- Operational restructuring.

The company also increased efforts to modernize its digital insurance systems and improve internal operational controls.

Combs became closely associated with efforts to restore stronger underwriting profitability after periods of elevated insurance losses.

GEICO Executive Management Structure

GEICO’s daily operations are managed through a large executive and operational leadership structure.

Key operational areas include:

Underwriting Leadership

Underwriting executives control policy pricing, customer risk selection, and insurance approval standards.

These teams play a critical role in profitability because poor underwriting decisions can create major financial losses.

For example, if accident rates rise sharply in certain states, underwriting teams may adjust pricing models or reduce exposure in those regions.

Claims Management Teams

Claims divisions manage accident investigations, payouts, fraud detection, and settlement operations.

Efficient claims handling is essential in the insurance industry because claims expenses directly affect profitability.

GEICO invests heavily in claims automation and digital processing systems to improve operational speed.

Technology and Digital Operations

Technology leadership became increasingly important as GEICO expanded its digital-first insurance strategy.

The company invests heavily in:

- Mobile applications

- Online policy systems

- Claims automation

- AI-driven insurance processing tools

- Customer service infrastructure.

This technology-focused strategy helps GEICO compete against both traditional insurers and newer digital insurance companies.

Marketing and Customer Acquisition

Marketing executives oversee one of the largest advertising operations in the insurance industry.

GEICO became famous for large-scale advertising campaigns including:

- The GEICO Gecko

- Caveman commercials

- Sports sponsorships

- National television advertising.

The company’s aggressive advertising strategy helped transform GEICO into one of the most recognized insurance brands in the United States.

Role of Berkshire Hathaway Insurance Operations

GEICO also operates within Berkshire Hathaway’s broader insurance ecosystem.

Berkshire controls multiple insurance businesses including:

- General Re

- National Indemnity Company

- Berkshire Hathaway Reinsurance Group.

This creates additional oversight from Berkshire’s insurance leadership structure.

Insurance operations within Berkshire Hathaway often share broader strategic philosophies related to underwriting discipline and capital management.

How Decision-Making Works at GEICO

Decision-making at GEICO combines operational independence with parent-company oversight.

Daily operational decisions are usually handled internally by GEICO executives.

These decisions include:

- Pricing adjustments

- Claims operations

- Hiring strategies

- Marketing campaigns

- Technology investments.

Larger strategic decisions may involve Berkshire Hathaway leadership approval, especially when significant capital allocation or operational restructuring is involved.

This balance allows GEICO to react quickly to insurance market conditions while still benefiting from Berkshire Hathaway’s long-term strategic guidance.

How Control Impacts GEICO’s Market Strategy

The control structure affects how GEICO competes in the insurance market.

Because Berkshire Hathaway prioritizes long-term stability, GEICO can sometimes make strategic decisions that differ from publicly traded competitors facing short-term shareholder pressure.

For example, during periods of high claims inflation, GEICO may prioritize underwriting profitability over aggressive market share growth.

This long-term control structure helps the company maintain financial discipline even during volatile insurance cycles.

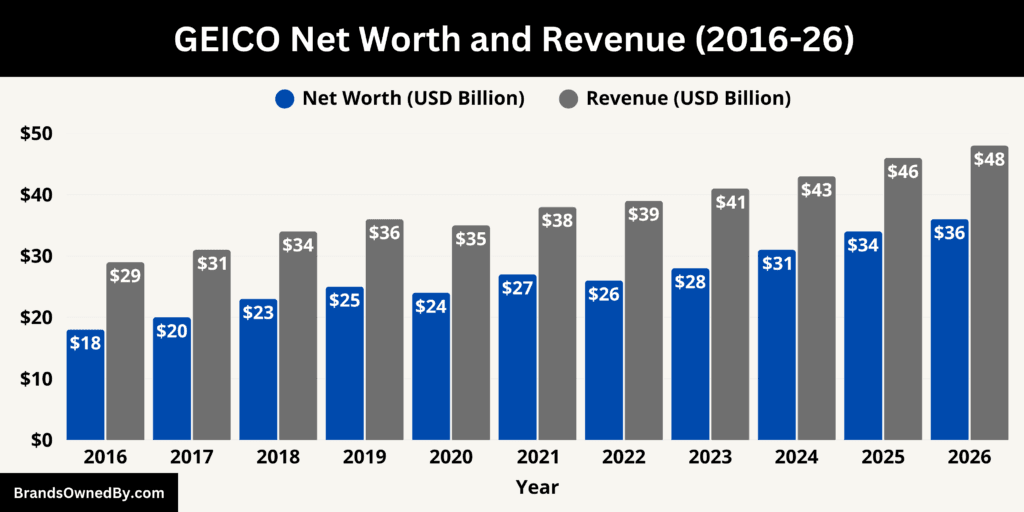

GEICO Annual Revenue and Net Worth

As of April 2026, GEICO is estimated to generate approximately $48 billion in annual revenue, making it one of the largest automobile insurance companies in the United States. The company’s estimated enterprise value and net worth stand at roughly $36 billion based on underwriting profitability, premium growth, market share, policyholder scale, and long-term earnings potential.

The company strengthened its financial position significantly between 2023 and 2025 after implementing aggressive underwriting reforms, pricing increases, operational restructuring, and technology modernization initiatives.

Recent financial disclosures tied to Berkshire Hathaway’s insurance operations showed GEICO generated approximately $45.2 billion in written premiums during 2025 while producing nearly $6.8 billion in pre-tax underwriting profit.

Those figures positioned GEICO among the most profitable personal auto insurance businesses in North America.

GEICO Revenue Breakdown in 2026

GEICO’s estimated 2026 revenue of $48 billion is primarily driven by personal auto insurance premiums.

The company’s revenue model is heavily concentrated around direct-written automobile insurance policies sold across the United States.

The estimated revenue composition in 2026 includes:

| Revenue Segment | Estimated 2026 Revenue | Share of Total Revenue |

|---|---|---|

| Personal Auto Insurance | $39.5 billion | 82.3% |

| Commercial Auto Insurance | $3.2 billion | 6.7% |

| Motorcycle & Specialty Vehicle Insurance | $1.4 billion | 2.9% |

| Partner Insurance Products | $2.1 billion | 4.4% |

| Policy Fees & Other Insurance Services | $1.8 billion | 3.7% |

Personal auto insurance remains the company’s dominant business segment.

This includes liability coverage, collision insurance, comprehensive insurance, uninsured motorist protection, and medical coverage policies.

Commercial auto insurance also became an increasingly important growth segment due to expansion in delivery fleets, contractor vehicle coverage, and small business transportation services.

The company’s partner insurance business generates additional income through referral partnerships tied to homeowners insurance, renters insurance, and umbrella insurance products.

Premium Growth and Policy Expansion

GEICO’s premium growth accelerated after major pricing adjustments implemented between 2023 and 2025.

During 2025, written premiums increased by approximately 5.3% year-over-year to more than $45.2 billion.

This growth was driven by:

- Higher average premiums per policy

- Growth in policies-in-force

- Rate increases across multiple states

- Improved underwriting selection

- Recovery in customer acquisition campaigns.

The company also resumed more aggressive advertising spending after previously reducing marketing intensity during profitability restructuring periods.

Reports from 2025 showed underwriting expenses increased sharply partly because GEICO expanded advertising and policy acquisition spending again.

Underwriting Profitability in 2026

One of the most important indicators of GEICO’s financial strength is underwriting profit.

Underwriting profit measures how much money an insurer keeps after paying claims and operational insurance expenses.

GEICO reported approximately $6.824 billion in pre-tax underwriting earnings for 2025.

The company’s combined ratio reached approximately 84.7% during 2025.

In insurance, a combined ratio below 100% means the insurer is generating underwriting profit.

An 84.7% combined ratio means GEICO spent roughly 84.7 cents on claims and operating expenses for every $1 collected in premiums.

That left strong underwriting margins despite rising claims severity and operational costs.

Claims Costs and Expense Structure

GEICO’s financial performance was heavily influenced by claims inflation between 2022 and 2025.

Vehicle repair costs increased substantially because of:

- Supply chain disruptions

- Higher auto part prices

- Advanced vehicle repair technology costs

- Labor inflation in repair shops

- Increased medical claim expenses.

During 2025, GEICO’s losses and loss adjustment expenses rose to approximately $32.1 billion.

At the same time, underwriting expenses increased more than 34% due to higher customer acquisition and advertising costs.

Despite these pressures, the company maintained strong profitability because of pricing increases and improved underwriting discipline.

GEICO Net Worth in 2026

As of 2026, GEICO’s estimated net worth and enterprise valuation stand near $36 billion.

This valuation is supported by several measurable business factors.

The company controls one of the largest personal auto insurance customer bases in the United States.

It also maintains extremely high brand recognition due to decades of national advertising campaigns.

Additional valuation drivers include:

| Valuation Factor | Estimated Impact on Enterprise Value |

|---|---|

| Insurance Premium Volume | Very High |

| Underwriting Profitability | Very High |

| Brand Recognition | High |

| Customer Retention Base | High |

| Digital Insurance Infrastructure | Moderate to High |

| Market Share Position | High |

| Berkshire Hathaway Ownership Stability | High |

GEICO’s integration within Berkshire Hathaway also strengthens its long-term financial stability.

The company contributes significant insurance float to Berkshire Hathaway’s broader investment operations.

Insurance float refers to premium money collected before claims are paid out.

That float creates additional long-term financial value for Berkshire Hathaway.

Why GEICO’s Revenue Continues Growing

Several structural advantages continue supporting GEICO’s financial growth.

The company operates one of the largest direct-to-consumer insurance models in the industry.

Unlike insurers that depend heavily on local agents, GEICO reduces distribution costs through centralized operations and digital sales systems.

The company also invested heavily in:

- Claims automation systems

- AI-assisted underwriting tools

- Mobile insurance applications

- Digital claims management

- Customer self-service platforms.

Operational restructuring also improved efficiency.

GEICO significantly reduced workforce size between 2020 and 2024 before selectively rebuilding staffing levels during 2025.

These changes helped improve operational margins.

GEICO Revenue Forecast Through 2030

GEICO’s future revenue growth will likely depend on premium pricing trends, customer retention performance, claims inflation management, and competitive positioning against rivals such as Progressive Corporation and State Farm.

Industry analysts expect continued revenue expansion because personal auto insurance premiums across the U.S. market remain elevated after several years of industry-wide pricing increases.

Projected revenue forecasts for GEICO include:

- 2027: Estimated revenue of $51 billion driven by higher premium renewals and expanded policy growth

- 2028: Estimated revenue of $54 billion supported by digital insurance expansion and improved retention rates

- 2029: Estimated revenue of $58 billion as AI-driven underwriting systems improve pricing precision and profitability

- 2030: Estimated revenue of $62 billion supported by market expansion, telematics adoption, and continued premium inflation adjustments.

Future profitability will depend heavily on how effectively GEICO controls claims severity, manages catastrophe exposure, and competes against increasingly technology-driven insurance rivals.

Brands Owned by GEICO

Unlike some insurance groups that operate dozens of separately branded insurance subsidiaries, GEICO runs a far more centralized brand structure.

The company primarily operates under the GEICO brand umbrella rather than maintaining a massive portfolio of independent consumer-facing insurance brands.

However, GEICO still controls multiple licensed insurance entities, underwriting companies, service divisions, and branded insurance operations that support its nationwide business infrastructure.

As of 2026, these entities collectively help GEICO manage underwriting risk, policy issuance, customer servicing, claims operations, and specialty insurance programs across different insurance categories.

| Company / Entity | Type | Primary Function | Key Details as of 2026 |

|---|---|---|---|

| Government Employees Insurance Company | Core Insurance Entity | Personal auto insurance underwriting | Original GEICO operating company founded in 1936. Handles a major portion of GEICO’s nationwide auto insurance business and premium generation. |

| GEICO General Insurance Company | Underwriting Subsidiary | Higher-risk and non-standard auto insurance coverage | Supports underwriting segmentation and risk management across different customer categories and state markets. |

| GEICO Indemnity Company | Insurance Subsidiary | Auto insurance policy underwriting and liability management | Helps distribute underwriting exposure and supports regulatory compliance across multiple U.S. jurisdictions. |

| GEICO Casualty Company | Insurance Subsidiary | Casualty insurance underwriting operations | Supports policy issuance and claims liability management within GEICO’s insurance structure. |

| GEICO Secure Insurance Agency | Insurance Agency Entity | Third-party insurance product distribution | Connects customers with partner insurance providers for homeowners, renters, condo, and specialty insurance products. |

| GEICO Motorcycle | Specialty Insurance Brand | Motorcycle insurance services | Provides motorcycle coverage including collision protection, roadside assistance, and accessory coverage. |

| GEICO Commercial Auto | Commercial Insurance Division | Business vehicle insurance coverage | Serves contractors, delivery operators, rideshare drivers, and commercial fleet businesses. |

| GEICO Marine Insurance | Specialty Insurance Brand | Boat and watercraft insurance | Provides insurance for boats, yachts, jet skis, and personal watercraft customers. |

| GEICO Digital Platform | Digital Insurance Infrastructure | Online insurance and claims management systems | Supports policy purchases, AI-assisted underwriting, digital claims filing, and customer self-service operations. |

| GEICO Gecko | Advertising Brand Asset | Marketing and customer acquisition | One of the most recognized advertising mascots in the U.S. insurance industry and a major contributor to brand recognition. |

Government Employees Insurance Company (GEICO)

Government Employees Insurance Company is the core legal insurance entity behind the GEICO brand.

This entity traces its origins back to 1936 when the company was originally created to serve government employees and military personnel.

Today, it functions as one of the primary underwriting and operating entities within GEICO’s insurance structure.

The company underwrites millions of private passenger auto insurance policies across the United States.

It remains the central operational backbone of GEICO’s insurance business and continues generating the majority of the company’s premium revenue.

The entity became especially important because of its direct-to-consumer insurance model, which reduced dependency on traditional insurance agents and lowered operating costs.

GEICO General Insurance Company

GEICO General Insurance Company operates as one of GEICO’s major underwriting subsidiaries.

This entity primarily focuses on higher-risk and non-standard auto insurance segments.

Insurance companies often separate underwriting entities based on risk profiles and regulatory structures.

GEICO General Insurance Company helps the broader organization manage pricing structures and underwriting exposure more efficiently.

The company supports policy issuance in multiple states and allows GEICO to segment customer risk categories more effectively.

This structure helps improve underwriting discipline and regulatory compliance across different insurance markets.

GEICO Indemnity Company

GEICO Indemnity Company is another important underwriting entity within GEICO’s corporate structure.

This subsidiary plays a significant role in issuing automobile insurance policies and managing insurance liabilities.

The company supports GEICO’s nationwide expansion by helping distribute underwriting exposure across multiple regulated insurance entities.

This structure is common in the insurance industry because it allows companies to manage risk concentration more efficiently while meeting state-level regulatory requirements.

GEICO Indemnity Company remains one of the most important operational entities supporting GEICO’s auto insurance business.

GEICO Casualty Company

GEICO Casualty Company operates as an additional underwriting and insurance entity within the broader GEICO structure.

The company helps support underwriting operations for specific insurance risk categories and regional insurance markets.

Like other GEICO underwriting subsidiaries, it contributes to policy issuance and claims liability management.

This multi-entity structure gives GEICO greater flexibility in pricing models, underwriting segmentation, and regulatory compliance strategies.

GEICO Secure Insurance Agency

GEICO Secure Insurance Agency operates differently from GEICO’s underwriting companies.

Instead of directly underwriting all insurance products itself, this entity functions as an insurance agency platform that connects customers with third-party insurance providers.

The agency supports products such as:

- Homeowners insurance

- Condo insurance

- Renters insurance

- flood insurance

- identity theft protection.

This structure allows GEICO to expand into additional insurance categories without assuming all underwriting risks directly.

The agency model also creates additional commission and partnership revenue streams for the company.

GEICO Marine Insurance Operations

GEICO also operates branded marine insurance programs for recreational watercraft customers.

These operations support insurance products for:

- Boats

- Yachts

- Personal watercraft

- Fishing vessels

- Sailboats.

Marine insurance became an important niche segment within GEICO’s broader specialty insurance offerings.

The business expanded as recreational boating activity increased across coastal and vacation markets in the United States.

GEICO Motorcycle Brand

GEICO Motorcycle operates as a specialized branded insurance segment targeting motorcycle owners.

The company markets these policies separately because motorcycle insurance involves different underwriting risks compared to traditional passenger vehicles.

Coverage products include:

- Collision protection

- Helmet and accessory coverage

- Emergency roadside assistance

- Medical payment coverage.

The motorcycle insurance segment also supports customer diversification beyond standard auto insurance policies.

GEICO Commercial Auto Division

GEICO Commercial Auto functions as a specialized insurance entity focused on business-related vehicle coverage.

The division serves:

- Small businesses

- Contractors

- Delivery companies

- Rideshare operators

- Commercial fleets.

This segment became increasingly important as delivery-based businesses and gig economy transportation services expanded during the 2020s.

Commercial auto insurance also generates higher-value policy opportunities compared to many standard personal auto policies.

GEICO Digital Insurance Platforms

One of GEICO’s most valuable operational assets is its digital insurance infrastructure ecosystem.

Although not a standalone public-facing brand, these technology platforms became critical operational entities within the company.

The systems support:

- Online policy purchases

- AI-assisted underwriting

- Mobile claims processing

- Customer self-service systems

- automated claims assessment

- digital ID verification.

As of 2026, GEICO continued investing heavily in digital transformation initiatives to compete more aggressively with technology-driven insurance rivals.

These systems also help reduce operating costs compared to insurers that rely heavily on physical agent networks.

GEICO Advertising Brand Assets

GEICO also controls several major intellectual property and advertising assets connected to its marketing operations.

The company’s advertising campaigns became some of the most recognizable in the insurance industry.

Major brand assets include:

- The GEICO Gecko

- Caveman advertising campaigns

- Branded sports sponsorships

- National advertising partnerships.

These advertising properties helped GEICO build nationwide brand recognition and customer acquisition scale.

Marketing operations remain central to GEICO’s long-term growth strategy.

Conclusion

Understanding who owns GEICO reveals why the company operates differently from many competitors. GEICO is fully owned by Berkshire Hathaway, the multinational conglomerate led for decades by Warren Buffett.

That ownership structure gives GEICO strong financial backing and long-term operational stability. It also allows the company to focus on disciplined growth rather than short-term market pressure.

Over the years, GEICO evolved from a niche insurer serving government employees into one of the most recognized insurance brands in America. Its direct-sales model, aggressive marketing, and Berkshire Hathaway backing helped drive that transformation.

FAQs

Is GEICO publicly traded?

No, GEICO is not a publicly traded company. The insurer was fully acquired by Berkshire Hathaway in 1996 and now operates as a wholly owned subsidiary within Berkshire Hathaway’s insurance division.

Because GEICO is privately held under Berkshire Hathaway, investors cannot buy GEICO stock directly on the stock market. Instead, investors who want exposure to GEICO must purchase shares of Berkshire Hathaway, which owns the company entirely.

What does GEICO stand for?

GEICO stands for Government Employees Insurance Company.

The name reflects the company’s original business strategy when it was founded in 1936 by Leo Goodwin Sr. and Lillian Goodwin.

At the time, the company focused primarily on providing auto insurance to U.S. government employees and military personnel. The founders believed government workers represented lower-risk customers because of stable employment and predictable driving behavior.

Although GEICO later expanded into the mainstream insurance market, the original name remained part of the brand identity.

Is GEICO owned by Allstate?

No, GEICO is not owned by Allstate.

The two companies are direct competitors in the U.S. insurance industry. GEICO is fully owned by Berkshire Hathaway, while Allstate operates as a separate publicly traded insurance corporation owned by institutional and retail shareholders.

Both companies compete aggressively in areas such as:

- Auto insurance

- Digital insurance services

- Customer acquisition

- Advertising campaigns

- Claims processing technology.

Who is GEICO affiliated with?

GEICO is affiliated primarily with Berkshire Hathaway, its parent company and sole owner.

Through Berkshire Hathaway, GEICO is connected to a broader network of insurance and financial operations that include businesses such as:

- General Re

- National Indemnity Company

- Berkshire Hathaway Reinsurance Group.

The company also works with third-party insurance partners through entities like GEICO Secure Insurance Agency for products such as homeowners insurance, renters insurance, and specialty insurance coverage.

Is GEICO government owned?

No, GEICO is not owned or operated by the U.S. government.

Many people assume the company has government ownership because of its name. However, the word “Government” in GEICO simply reflects the company’s original target customer base when it was founded.

Today, GEICO is a privately controlled insurance company fully owned by Berkshire Hathaway.

The company operates as a commercial insurance business serving millions of customers across the United States.

Is GEICO a private company?

Yes, GEICO operates as a private company under the ownership of Berkshire Hathaway.

Before 1996, GEICO traded publicly on the stock market. However, after Berkshire Hathaway completed its full acquisition of the insurer, GEICO became privately held.

This ownership structure gives GEICO more long-term operational flexibility because the company does not face direct pressure from public shareholders focused on quarterly earnings performance.

Who is the majority owner of GEICO?

Berkshire Hathaway is the majority owner and full owner of GEICO.

The conglomerate owns 100% of the company after completing its acquisition in 1996.

Because Berkshire Hathaway fully controls GEICO, it has authority over major strategic decisions, capital allocation, executive oversight, and long-term operational direction.

GEICO now operates as one of Berkshire Hathaway’s most important insurance subsidiaries.

Does Warren Buffett own GEICO insurance?

Warren Buffett indirectly owns GEICO through his large ownership stake and leadership control of Berkshire Hathaway.

Buffett played a major role in GEICO’s history long before Berkshire Hathaway fully acquired the company.

He first became interested in GEICO during the 1950s after studying its direct-to-consumer insurance model. Later, during GEICO’s financial crisis in the 1970s, Buffett invested heavily in the company through Berkshire Hathaway.

That investment eventually became one of Berkshire Hathaway’s most successful long-term acquisitions.

Does Berkshire Hathaway own GEICO?

Yes, Berkshire Hathaway fully owns GEICO.

Berkshire Hathaway gradually increased its ownership stake in GEICO over several decades before completing the full acquisition in 1996 in a deal valued at approximately $2.3 billion.

Since then, GEICO has operated as a wholly owned Berkshire Hathaway subsidiary.

The acquisition gave GEICO access to Berkshire Hathaway’s massive financial resources and long-term investment strategy, helping the company expand aggressively in advertising, digital insurance technology, and nationwide customer growth.