- Wells Fargo is a publicly traded company owned by shareholders, with no single individual or entity having controlling ownership.

- Institutional investors dominate ownership, holding over 84% of total shares, led by The Vanguard Group and BlackRock.

- The largest shareholder, Vanguard, owns about 9.5% (350M+ shares), followed by BlackRock with 8% stake, but both act as passive investors.

- Ownership is highly diversified across thousands of institutions and millions of investors, while actual control is exercised by the CEO, board of directors, and regulators.

Wells Fargo & Company is one of the most established banking institutions in the United States. It was founded in 1852 during the California Gold Rush. The company built its reputation by providing banking and express delivery services to miners, merchants, and settlers.

Today, Wells Fargo operates as a diversified financial services firm. It offers retail banking, commercial banking, wealth management, and investment services. The bank serves individuals, small businesses, and large corporations. Its operations are spread across thousands of branches and digital platforms.

Wells Fargo is widely recognized for its strong presence in consumer banking. It has also built a large footprint in mortgage lending and small business financing. Over time, the company has shifted toward digital banking while maintaining its traditional branch network.

It remains one of the “Big Four” banks in the U.S., competing with JPMorgan Chase, Bank of America, and Citigroup.

Founders of Wells Fargo

Wells Fargo was founded by two influential businessmen: Henry Wells and William G. Fargo.

Henry Wells

Henry Wells was an experienced entrepreneur in the financial and logistics sectors. Before co-founding Wells Fargo, he played a key role in establishing express delivery services in the United States. He was also involved in founding American Express.

Wells believed in combining banking with transportation services. This idea became the foundation of Wells Fargo’s early success. His vision helped the company expand quickly during the Gold Rush era.

William G. Fargo

William G. Fargo was a business partner of Henry Wells and an expert in logistics and operations. He also co-founded American Express. Fargo focused on building efficient delivery networks and reliable financial services.

His leadership helped Wells Fargo gain trust among customers. He ensured that money, gold, and valuable goods were transported safely across long distances.

Founders’ Legacy

Together, Henry Wells and William G. Fargo created a company that blended banking with express services. This model was innovative for its time. It allowed Wells Fargo to grow rapidly in a challenging environment.

Their legacy still shapes the company today. The focus on customer trust, reliability, and nationwide service remains central to Wells Fargo’s identity.

Ownership History

The ownership history of Wells Fargo & Company shows a clear evolution from tightly controlled founder ownership to a highly diversified institutional structure. As of April 2026, ownership is widely distributed, with institutional investors dominating the shareholder base.

Early Founder and Private Ownership (1852–1900s)

When Wells Fargo was founded in 1852, ownership was concentrated among its founders, Henry Wells and William G. Fargo, along with a small group of private investors.

The company operated as a privately held business. Decision-making power and ownership were closely aligned. This allowed rapid expansion during the Gold Rush, especially in banking and logistics.

Over time, additional investors joined. However, ownership remained limited and concentrated.

Transition to Public Ownership

As Wells Fargo expanded into a national banking institution, it transitioned into a publicly traded company. This shift allowed it to raise capital from a broader investor base.

Ownership began to spread across thousands of shareholders. A formal governance structure was introduced. This included a board of directors and shareholder voting rights.

The company adopted a one-share, one-vote system, meaning voting power directly reflects share ownership.

This marked the beginning of modern corporate ownership for Wells Fargo.

Transformational Mergers That Reshaped Ownership

Ownership changed significantly through major mergers.

The 1998 merger with Norwest Corporation was a defining moment. Norwest technically acquired Wells Fargo. However, the combined entity kept the Wells Fargo name due to its stronger brand value.

This merger brought in a new shareholder base. Norwest investors became key stakeholders in the newly structured company.

Another major shift occurred in 2008 when Wells Fargo acquired Wachovia during the financial crisis.

This deal:

- Expanded Wells Fargo’s national presence

- Added millions of new customers

- Introduced a large pool of new institutional shareholders.

These mergers significantly diluted any concentrated ownership and moved the company toward a fully diversified shareholder base.

Rise of Institutional Dominance (2010s–2026)

In recent decades, institutional investors have become the dominant owners of Wells Fargo.

As of 2026:

- Institutional investors hold over 75% of total shares

- In some estimates, this figure exceeds 83% of total ownership

The largest shareholders include:

- The Vanguard Group — about 9.6% ownership

- BlackRock — over 6% stake

- Fidelity Investments — around 6% ownership

- State Street Corporation — about 4.4% stake.

These firms manage funds on behalf of millions of investors. This means indirect ownership is spread globally across pension funds, ETFs, and retail portfolios.

There are also thousands of institutional holders overall. More than 3,000 institutions hold shares in Wells Fargo.

Decline of Individual Dominance

Unlike earlier decades, no individual investor controls Wells Fargo today. Even historically large individual stakeholders have reduced influence over time.

Ownership is now fragmented. No single shareholder holds a controlling stake. Even the largest investor, Vanguard, owns less than 10%.

Retail investors also play a role. A meaningful portion of shares is held by individual investors through brokerage accounts and retirement funds.

Modern Ownership Structure (2026)

As of 2026, Wells Fargo represents a classic example of a modern publicly traded corporation:

- Ownership is highly decentralized

- Institutional investors dominate voting power

- Retail investors hold a smaller but meaningful share

- Insider ownership remains minimal (less than 1%).

This structure ensures liquidity and stability. It also means that influence is exercised collectively through shareholder voting rather than by a single controlling entity.

Who Owns Wells Fargo: Major Shareholders

Wells Fargo & Company is a publicly traded bank. It is owned by shareholders rather than a single individual or family. As of April 2026, ownership is highly institutionalized and widely distributed.

Wells Fargo has approximately 3.7 billion outstanding shares. A large majority of these shares are held by institutional investors. In fact, institutional ownership exceeds 84% of total shares, while insider ownership remains below 0.1%.

This means control is not concentrated. Instead, ownership is spread across asset managers, pension funds, ETFs, and millions of retail investors. The largest shareholders are global investment firms that manage money on behalf of clients.

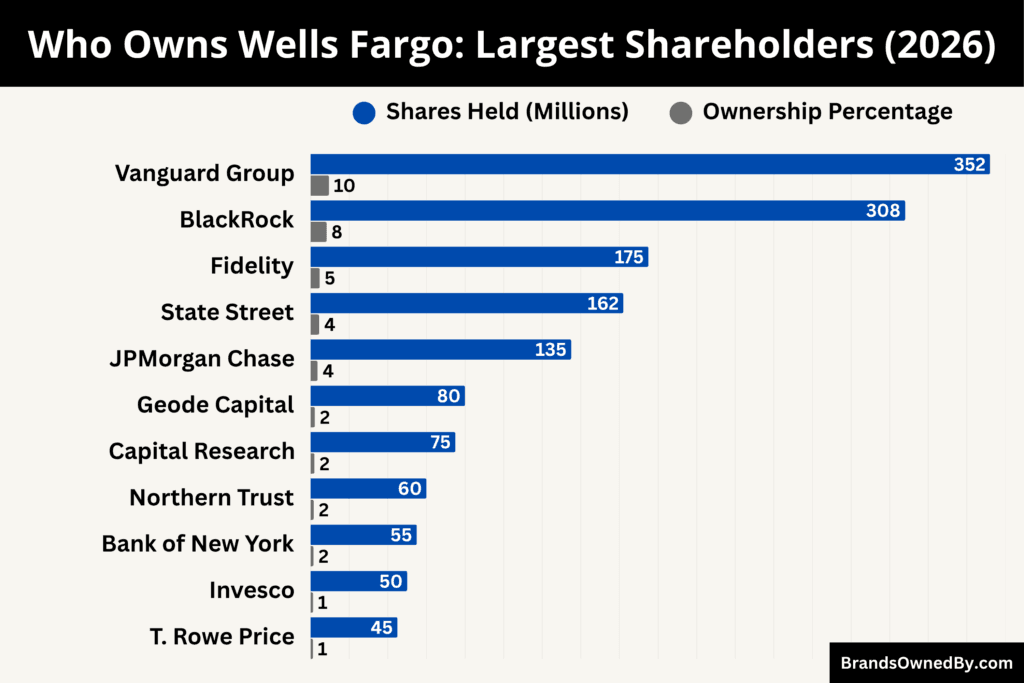

The Vanguard Group

The Vanguard Group is the largest shareholder of Wells Fargo.

It holds approximately 350 million to 355 million shares, representing about 9.5% to 9.6% ownership of the company.

Vanguard’s position is built through its index funds and ETFs. These include funds that track the S&P 500 and the total U.S. stock market. Because Wells Fargo is a major component of these indices, Vanguard maintains a large and stable stake.

Although Vanguard does not actively manage Wells Fargo, it plays a significant governance role. It votes on board appointments, executive compensation, and corporate policies. Its long-term investment strategy makes it one of the most influential shareholders.

BlackRock

BlackRock is the second-largest shareholder.

BlackRock owns roughly 300 million to 315 million shares, giving it about 8.1% to 8.5% ownership in Wells Fargo.

Its holdings are spread across its iShares ETF lineup and institutional portfolios. BlackRock’s scale gives it considerable voting power in shareholder meetings.

The firm is known for engaging with companies on governance and risk management. In Wells Fargo’s case, BlackRock has supported efforts to strengthen compliance and oversight following past regulatory challenges.

Fidelity Investments (FMR LLC)

Fidelity Investments is another major shareholder.

Fidelity holds approximately 170 million to 180 million shares, representing around 4.6% to 4.8% ownership.

Unlike Vanguard and BlackRock, Fidelity combines passive and active investment strategies. Some of its funds actively choose to invest in Wells Fargo based on performance expectations.

This gives Fidelity a more flexible role. It can increase or reduce its stake depending on market conditions. Its voting influence remains significant, especially in matters related to corporate governance.

State Street Corporation

State Street Corporation is one of the largest passive investors in Wells Fargo.

It owns around 160 million to 165 million shares, which equals roughly 4.3% to 4.4% ownership.

State Street’s holdings are largely tied to index funds and ETFs such as the SPDR S&P 500 ETF. Because of this, its investment is relatively stable over time.

Despite being a passive investor, State Street plays an active role in voting and governance. It often focuses on board diversity, transparency, and long-term shareholder value.

JPMorgan Asset Management

JPMorgan Chase, through its asset management division, is also a significant shareholder.

It holds approximately 120 million to 150 million shares, representing about 3.2% to 4.0% ownership.

This stake is distributed across mutual funds, institutional mandates, and advisory portfolios. While smaller than the top three shareholders, JPMorgan’s position is still influential in shareholder decisions.

Its investment approach blends active and passive strategies, allowing it to adjust exposure based on market trends and banking sector outlook.

Other Institutional Shareholders

Beyond the top five, Wells Fargo has a very broad institutional base.

More than 3,000 institutional investors collectively hold over 3.1 billion shares. These include:

- Pension funds

- Insurance companies

- Sovereign wealth funds

- Hedge funds and asset managers.

Individually, these firms hold smaller stakes. However, together they represent the majority of ownership. This creates a highly diversified shareholder structure.

No single institution has controlling power. Even the largest shareholder owns less than 10%.

Retail and Individual Investors

Retail investors hold a smaller but still meaningful portion of Wells Fargo shares.

This group includes:

- Individual investors buying shares directly

- Employees receiving stock-based compensation

- Investors holding shares through retirement accounts.

Combined, retail investors own roughly 15% or less of total shares, which equals hundreds of millions of shares.

While they lack coordinated influence, they contribute to overall market liquidity and shareholder diversity.

Insider Ownership

Insider ownership at Wells Fargo is minimal.

Executives and board members collectively hold less than 3 million shares, representing under 0.1% of total ownership.

This is typical for large U.S. banks. It reflects a clear separation between ownership and management. Executives are incentivized through compensation and performance-based stock awards rather than large ownership stakes.

Competitor Ownership Comparison

Wells Fargo’s ownership structure is not unique. It reflects a broader pattern across the U.S. banking industry, where large institutional investors dominate shareholding. However, when compared closely with competitors, differences appear in ownership concentration, shareholder mix, and influence.

| Bank | Institutional Ownership (%) | Largest Shareholder | Stake (%) | Second Largest Shareholder | Stake (%) | Top 2 Combined (%) | Ownership Concentration | Insider Ownership |

|---|---|---|---|---|---|---|---|---|

| Wells Fargo & Company | 84% | The Vanguard Group | 9.5% | BlackRock | 8.3% | 17.8% | Slightly higher concentration among top holders | <0.1% |

| JPMorgan Chase | 78% | The Vanguard Group | 9.0% | BlackRock | 7.5% | 16.5% | More diversified beyond top investors | <1% |

| Bank of America | 73% | The Vanguard Group | 8.6% | BlackRock | 7.6% | 16.2% | Broad shareholder base | <1% |

| Citigroup | 77% | The Vanguard Group | 8.5% | BlackRock | 7.8% | 16.3% | Balanced institutional ownership | <1% |

| Goldman Sachs | 76% | The Vanguard Group | 8.0% | BlackRock | 6.5% | 14.5% | Lower concentration than Wells Fargo | 1% |

| Morgan Stanley | 75% | The Vanguard Group | 8.2% | BlackRock | 7.5% | 15.7% | Moderately concentrated | 1% |

| U.S. Bancorp | 76% | The Vanguard Group | 8.0% | BlackRock | 7.0% | 15.0% | More distributed ownership | <1% |

Comparison with Big Four Banks

JPMorgan Chase, Bank of America, and Citigroup share a nearly identical ownership framework with Wells Fargo.

All four banks are publicly traded and primarily owned by institutional investors. Wells Fargo has slightly higher institutional ownership at around 84%, while JPMorgan, Citigroup, and Bank of America range between roughly 73% and 80%.

The same three firms dominate ownership across all four banks:

- The Vanguard Group

- BlackRock

- State Street Corporation.

In Wells Fargo, Vanguard holds about 352M shares (9.5%) and BlackRock about 308M shares (8.3%). This combined stake of nearly 18% is slightly higher than what is typically seen in JPMorgan and Citigroup, where top two shareholders usually hold a slightly smaller combined percentage.

This indicates that Wells Fargo has marginally higher ownership concentration among its largest investors.

Ownership Concentration Differences

While all major banks have diversified ownership, the degree of concentration varies.

Wells Fargo’s top three shareholders collectively hold over 22% of total shares. In comparison, competitors like JPMorgan and Bank of America have slightly more dispersed ownership beyond their top two investors.

This difference is small but important. A higher concentration means that a few large institutional investors have relatively greater voting influence in Wells Fargo compared to its peers.

However, no bank in this group has a controlling shareholder. Even the largest investors hold less than 10% individually, ensuring that control remains distributed.

Comparison with Investment Banks

Goldman Sachs and Morgan Stanley also follow the same institutional ownership model.

Vanguard and BlackRock are again the largest shareholders in both firms. Institutional ownership levels are generally between 75% and 80%, slightly lower than Wells Fargo.

The key difference lies in insider ownership. Investment banks tend to have higher insider stakes compared to Wells Fargo. Senior executives often hold more equity due to compensation structures tied to performance.

Wells Fargo, by contrast, has very low insider ownership, reinforcing a stronger separation between management and ownership.

Comparison with Regional Banks

Regional banks such as U.S. Bancorp provide another point of comparison.

These banks also have high institutional ownership, typically above 75%. However, their ownership is usually less concentrated among the top shareholders.

They often have:

- Greater participation from retail investors

- Slightly smaller stakes held by top institutional investors

- A more distributed shareholder base overall.

Compared to these banks, Wells Fargo has a more concentrated institutional ownership structure, with larger stakes held by its top investors.

Who Controls Wells Fargo?

Control of Wells Fargo & Company is exercised through a layered governance structure rather than a single owner. While millions of shareholders own the company, actual control lies with its executive leadership, board of directors, and regulatory framework. This separation ensures that a complex financial institution like Wells Fargo is managed professionally and under strict oversight.

CEO and Executive Leadership

The primary control of Wells Fargo’s day-to-day operations rests with its CEO, Charles W. Scharf.

Since taking over in 2019, Scharf has led a multi-year transformation of the bank. His role goes far beyond routine management. He is responsible for setting long-term strategic priorities, reshaping the bank’s structure, and ensuring compliance with regulatory requirements. Under his leadership, Wells Fargo has focused heavily on simplifying operations, reducing risk exposure, and strengthening internal controls.

The CEO works with a large executive leadership team that oversees core divisions such as consumer banking, corporate and investment banking, risk management, technology, and wealth management. These executives collectively manage thousands of employees and multiple business lines. However, final authority on major operational and strategic decisions flows through the CEO’s office.

In practical terms, this means that while shareholders own the company, the CEO and executive team determine how capital is allocated, which markets to prioritize, and how the bank responds to economic and regulatory challenges.

Board of Directors and Strategic Oversight

Above the executive team sits the board of directors, which plays a central role in controlling Wells Fargo at a strategic level.

The board does not manage daily operations. Instead, it provides oversight, sets governance standards, and ensures accountability. It represents shareholder interests and has the authority to appoint or remove the CEO, approve major strategic initiatives, and monitor risk.

Wells Fargo’s board has taken on an especially active role in recent years. Following regulatory scrutiny, the board has been deeply involved in strengthening governance practices, improving transparency, and ensuring compliance across the organization.

Board committees focus on critical areas such as audit, risk, compensation, and corporate governance. These committees review internal controls, approve executive pay structures, and evaluate whether management decisions align with long-term shareholder value.

This structure ensures that even though the CEO runs the company, their decisions are continuously reviewed and challenged at the board level.

Influence of Institutional Shareholders

Large institutional investors such as The Vanguard Group and BlackRock play an important but indirect role in controlling Wells Fargo.

These firms are the largest shareholders, collectively holding a significant percentage of the company’s shares. However, they do not participate in day-to-day management. Their influence is exercised through shareholder voting and ongoing engagement with the board and management.

They vote on key matters such as the election of directors, executive compensation policies, and major corporate proposals. In addition, they often hold private discussions with company leadership to express views on governance, risk management, and long-term strategy.

Because these firms manage funds on behalf of millions of investors, their approach is typically long-term and stability-focused. They aim to ensure that Wells Fargo is well-governed and financially sound rather than directly controlling its operations.

Regulatory Oversight and External Control

An essential layer of control over Wells Fargo comes from regulators. As one of the largest banks in the United States, it operates under strict supervision from bodies such as the Federal Reserve and other financial regulators.

This regulatory oversight directly shapes how the bank is run. Authorities set capital requirements, enforce risk controls, and monitor compliance with banking laws. Wells Fargo has faced regulatory restrictions in recent years, including limits on its asset growth. These constraints have had a direct impact on strategic decisions and operational priorities.

Unlike most industries, banks do not operate with full autonomy. Regulatory agencies have the power to approve or restrict certain actions, making them a critical part of the control structure.

Separation of Ownership and Control

Wells Fargo operates under a clear separation between ownership and control, which is typical for large publicly traded corporations.

Shareholders provide capital and hold voting rights, but they do not manage the business. The executive team runs the company, while the board ensures accountability. Regulators add an external layer of discipline.

This multi-layered structure reduces the risk of excessive concentration of power. It also ensures that decisions are made with oversight from multiple stakeholders.

Wells Fargo Annual Revenue and Net Worth

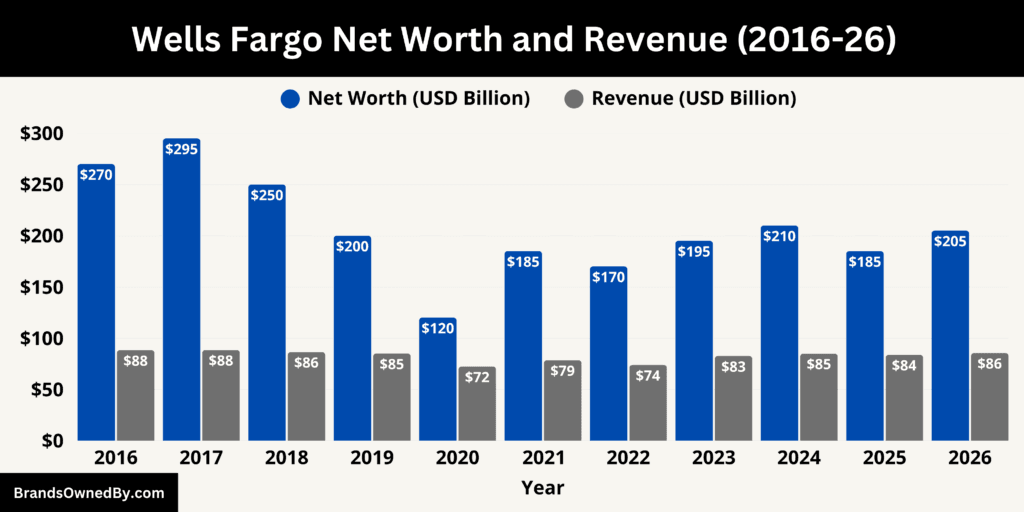

Wells Fargo & Company has stabilized its financial position as of April 2026, with annual revenue of $83.7 billion (2025 actual) and continued performance in a similar range for 2026. The bank’s net worth, measured by market capitalization, stands at approximately $200–$210 billion, supported by strong profitability, improved governance, and a balance sheet exceeding $2 trillion in assets.

This combination of stable revenue, rising net income, and strong capital position reflects a bank that has moved beyond its restructuring phase into consistent value generation.

Revenue Breakdown and Financial Performance (2025–2026)

Wells Fargo generated $83.7 billion in total revenue in 2025, driven primarily by net interest income and supported by fee-based business lines.

The bank’s revenue structure is dominated by net interest income, which is expected to reach around $50 billion annually going into 2026. This income is generated from loans, including mortgages, commercial lending, auto loans, and credit cards.

The second major component is non-interest income, which includes:

- Wealth and investment management fees

- Investment banking advisory revenues

- Trading and capital markets income

- Service charges and transaction fees.

Quarterly data reinforces this trend. In Q4 2025 alone, Wells Fargo reported $21.29 billion in revenue, showing steady year-over-year growth.

Overall, revenue growth is supported by rising loan volumes, improved credit quality, and expansion in fee-based services. The bank has also benefited from the removal of regulatory constraints, allowing it to expand operations and balance sheet capacity.

Net Income and Profitability

Profitability is a key driver of Wells Fargo’s net worth.

The bank reported $21.3 billion in net income for 2025, reflecting a 7% year-over-year increase.

This growth is driven by:

- Higher interest income due to elevated rates

- Improved efficiency and cost reductions

- Strong performance in consumer banking and wealth management.

Quarterly profits remain strong, with over $5.3 billion earned in Q4 2025 alone, indicating consistent earnings momentum.

This level of profitability supports shareholder returns, including dividends and stock buybacks, while also strengthening the bank’s capital base.

Net Worth Explained (Market Cap and Equity Value)

Wells Fargo’s net worth can be understood through two key metrics: market capitalization and shareholder equity.

As of 2026, the bank’s market capitalization is approximately $200–$210 billion. This reflects the total value investors assign to the company based on its earnings, growth potential, and risk profile.

Beyond market value, Wells Fargo’s book value (shareholder equity) is substantial. As of the end of 2025, the bank reported:

- Total assets: $2.1 trillion

- Loans: $986 billion

- Deposits: $1.4 trillion

- Shareholder equity: over $190 billion.

This means Wells Fargo’s intrinsic net worth, based on its balance sheet, is backed by real financial assets and capital reserves, not just stock market valuation.

The combination of high asset levels and strong equity provides stability and supports long-term growth.

Balance Sheet Strength and Capital Position

Wells Fargo’s balance sheet is one of the largest in the global banking sector.

With over $2.1 trillion in assets, the bank generates income through a wide lending base while maintaining strong liquidity through its deposit base.

Deposits of around $1.4 trillion provide low-cost funding. Loans of nearly $1 trillion generate interest income, forming the core of its business model.

Additionally, the bank has improved credit quality and reduced risk exposure in recent years. Lower charge-offs and stronger loan performance have contributed to stable earnings.

This balance sheet strength is a major factor behind Wells Fargo’s sustained valuation and financial resilience.

Revenue and Net Worth Trend (2016–2026)

Over the past decade, Wells Fargo has experienced a clear financial cycle.

Revenue remained strong between 2016 and 2019 but faced pressure due to regulatory issues. In 2020, both revenue and market value declined sharply due to the pandemic.

From 2021 onward, the bank entered a recovery phase. Revenue stabilized, and profitability improved significantly. By 2025–2026, Wells Fargo has returned to consistent earnings growth and stable valuation.

The recovery has been driven by operational restructuring, regulatory improvements, and favorable interest rate conditions.

Future Revenue Forecast (2026–2030)

Based on current financial trends and growth drivers, Wells Fargo is expected to continue steady expansion:

- 2026: $85 billion expected revenue with strong interest income contribution

- 2027: $87–$90 billion driven by loan growth and improved margins

- 2028: $90–$93 billion supported by wealth management and investment services

- 2029: $93–$96 billion with expansion in digital banking and fee income

- 2030: $95–$100 billion potential range with full operational optimization.

These projections reflect gradual growth rather than aggressive expansion, consistent with the bank’s conservative strategy.

Brands Owned by Wells Fargo

Wells Fargo & Company does not operate like a traditional conglomerate with dozens of independent brands. Instead, it owns a regulated network of legal entities, subsidiaries, and operating companies that collectively deliver its banking, lending, and financial services.

As of 2026, the company operates through four primary business segments—consumer banking, commercial banking, corporate & investment banking, and wealth & investment management.

Below are the actual companies, subsidiaries, and acquired entities that form Wells Fargo’s operational structure:

| Company / Entity | Type | Core Function | Status (2026) | Key Details |

|---|---|---|---|---|

| Wells Fargo Bank, N.A. | Banking Subsidiary | Retail, commercial, and corporate banking | Active (Core Entity) | Main operating bank; holds majority of assets and deposits; backbone of all banking operations |

| Wells Fargo Securities, LLC | Broker-Dealer / Investment Banking | Capital markets, underwriting, M&A advisory | Active | Handles institutional finance, trading, and corporate advisory services |

| Wells Fargo Clearing Services, LLC | Brokerage / Wealth Management | Brokerage execution and advisory services | Active | Legal entity behind Wells Fargo Advisors; manages client investment accounts |

| Wells Fargo Asset Finance, LLC | Specialized Finance Subsidiary | Equipment leasing and asset-based lending | Active (Streamlined) | Focused on structured finance; reduced exposure after asset sales |

| Wells Fargo Dealer Services | Auto Finance Subsidiary | Auto lending and dealer financing | Integrated | Brand phased out; operations merged into consumer lending division |

| Wells Fargo Corporate Trust Entities | Fiduciary / Trustee Entities | Bond trustee and structured finance services | Active | Provides institutional trust and administrative services |

| Wachovia | Acquired Bank | Retail banking, brokerage, financial services | Fully Integrated | Acquired in 2008; expanded U.S. footprint; operations absorbed into core entities |

| Norwest Corporation | Merged Bank Holding Company | Banking and financial services | Fully Integrated | 1998 merger formed modern Wells Fargo structure |

| Wells Fargo Financial | Consumer Finance Subsidiary | Personal loans and subprime lending | Largely Discontinued | Scaled down due to risk reduction strategy |

| Wells Fargo Rail | Transportation / Leasing Subsidiary | Railcar leasing and asset management | Divested | Sold in 2025–2026 as part of strategic restructuring |

| Allspring Global Investments (Former) | Asset Management Company | Investment management | Divested (Former Subsidiary) | Previously Wells Fargo Asset Management; now independent |

Wells Fargo Bank, N.A.

Wells Fargo Bank, N.A. is the main legal banking entity and the most important subsidiary of Wells Fargo.

It is a nationally chartered bank and serves as the core operating company through which most of Wells Fargo’s financial services are delivered. This includes retail banking, deposits, lending, mortgages, and credit cards.

This entity alone holds over $1.7 trillion in assets, making it one of the largest banks in the United States.

Nearly all customer-facing banking activities, including branches and digital banking, are legally housed under this subsidiary.

Wells Fargo Securities, LLC

Wells Fargo Securities, LLC is a registered broker-dealer and investment banking subsidiary.

It handles capital markets activities such as underwriting debt and equity, trading securities, and providing advisory services for mergers and acquisitions.

This entity is critical to Wells Fargo’s presence in corporate finance and institutional markets. It allows the bank to compete directly with investment banks like Goldman Sachs and Morgan Stanley.

Wells Fargo Clearing Services, LLC

Wells Fargo Clearing Services, LLC is the legal entity behind brokerage operations, commonly associated with Wells Fargo Advisors.

It is registered with U.S. regulators as a broker-dealer and investment advisor. This entity executes trades, manages brokerage accounts, and provides financial advisory services.

It plays a central role in wealth management operations and handles client assets across retail and institutional segments.

Wells Fargo Asset Finance, LLC

Wells Fargo Asset Finance, LLC is a specialized financing subsidiary focused on asset-based lending.

It provides financing solutions for equipment, infrastructure, and industrial assets. This includes leasing and structured finance for sectors such as transportation, energy, and manufacturing.

Historically, this unit expanded through acquisitions of GE Capital’s equipment finance businesses.

However, as of 2025–2026, Wells Fargo has been actively streamlining this segment, including selling parts of its rail leasing portfolio to focus on core banking.

Wells Fargo Dealer Services

Wells Fargo Dealer Services was a major auto lending subsidiary that provided financing through dealerships.

While the standalone brand has been phased out, the underlying operations continue within Wells Fargo’s consumer lending structure. The bank remains one of the largest auto lenders in the U.S.

This reflects a broader strategy of integrating subsidiaries into core operations rather than maintaining separate brand identities.

Wells Fargo Corporate Trust Entities

Wells Fargo operates multiple corporate trust and fiduciary entities under its institutional banking division.

These entities provide trustee services for bonds, structured finance products, and institutional clients. They act as intermediaries in capital market transactions, ensuring compliance and administration.

This business is highly specialized and generates stable fee-based income.

Wachovia

Wachovia was acquired by Wells Fargo in 2008.

This acquisition is one of the most important in the company’s history. It significantly expanded Wells Fargo’s presence, especially on the East Coast.

Although Wachovia no longer exists as a separate brand, its legal entities, infrastructure, and customer base were fully absorbed into Wells Fargo’s subsidiaries, particularly Wells Fargo Bank, N.A. and its brokerage operations.

Norwest Corporation

Norwest Corporation merged with Wells Fargo in 1998.

Technically, Norwest was the acquiring entity, but the combined company adopted the Wells Fargo name due to its stronger brand recognition.

This merger reshaped the company’s corporate structure and created the foundation for its modern banking operations.

Wells Fargo Financial

Wells Fargo Financial was a consumer finance subsidiary focused on personal loans and subprime lending.

Over time, this business was scaled down and largely discontinued as part of Wells Fargo’s effort to reduce risk and simplify operations.

While no longer a major active entity, it remains part of the company’s historical subsidiary structure.

Wells Fargo Rail

Wells Fargo Rail was a railcar leasing and transportation asset subsidiary.

This business was built through acquisitions, including GE Capital Rail Services.

As of 2025–2026, Wells Fargo has exited this business by selling its rail leasing portfolio.

This reflects a strategic shift toward focusing on core banking and reducing exposure to capital-intensive industries.

Allspring Global Investments

Allspring Global Investments was previously Wells Fargo Asset Management, a major investment management subsidiary.

Wells Fargo sold this business in 2021 to private equity firms, and it now operates independently.

Despite the sale, it remains relevant as a former core subsidiary that once managed over $600 billion in assets.

Conclusion

Wells Fargo is not owned by a single person or family. It is owned by millions of shareholders, with institutional investors holding the largest stakes. Firms like Vanguard and BlackRock dominate the ownership structure.

Control, however, lies with the executive team and board of directors. The CEO and leadership team shape the company’s strategy and direction.

This separation of ownership and control is typical for large publicly traded banks. It ensures accountability while allowing professional management to run daily operations.

FAQs

Who owns Wells Fargo bank?

Wells Fargo & Company is owned by its shareholders. The largest owners are institutional investors like The Vanguard Group and BlackRock. Millions of individual investors also own shares.

Who bought Wells Fargo bank?

No single entity bought Wells Fargo. It has grown through mergers and acquisitions. The most notable deals include the merger with Norwest Corporation in 1998 and the acquisition of Wachovia in 2008.

Does Chase own Wells Fargo?

No, JPMorgan Chase does not own Wells Fargo. They are separate companies and direct competitors in the U.S. banking industry.

Who owns Wells Fargo stock?

Wells Fargo stock is owned by institutional investors, mutual funds, ETFs, and retail investors. The largest holders include Vanguard, BlackRock, and State Street, but ownership is spread across millions of shareholders globally.

Who owns Wells Fargo Center?

The Wells Fargo Center in Philadelphia is not owned by Wells Fargo. It is owned by Comcast Spectacor. Wells Fargo only holds the naming rights.

Who is the majority owner of Wells Fargo?

There is no majority owner of Wells Fargo. The largest shareholder, Vanguard, owns about 9–10%, which is far below a controlling stake.

Does Warren Buffett still own Wells Fargo?

No, Warren Buffett (through Berkshire Hathaway) has exited his investment in Wells Fargo. Berkshire Hathaway sold its remaining shares by 2022.

Is Wells Fargo Chinese-owned?

No, Wells Fargo is not Chinese-owned. It is an American bank owned primarily by U.S.-based institutional investors and global shareholders.