- Olipop is a privately owned company where founders Ben Goodwin and David Lester remain the largest individual shareholders, with combined ownership around 29% and full operational control.

- Institutional investors including J.P. Morgan Growth Equity Partners and Greenoaks Capital collectively hold the majority stake (over 50%), but no single investor has controlling ownership.

- Control is structured, not concentrated: founders run day-to-day operations, while the board (including investor representatives) must approve major financial decisions like funding, expansion, or acquisition.

Olipop operates in the functional beverage segment. It produces prebiotic sodas designed to support digestive health. The brand replaces traditional high-sugar soft drinks with formulations built around plant fiber, botanicals, and natural ingredients.

The company’s core proposition is behavioral substitution. Instead of asking consumers to quit soda, it offers a familiar experience with improved nutritional value. For example, a consumer switching from a conventional cola to Olipop’s Vintage Cola still gets a similar taste profile but with significantly less sugar and added functional benefits.

Olipop’s product development is science-driven. The formulations are built around ingredients like cassava root fiber, chicory root, and marshmallow root. These are selected to support gut microbiome health while maintaining taste consistency.

Distribution strategy has also been critical. The brand scaled through premium grocery chains such as Whole Foods and later expanded into mass retail like Target. This allowed Olipop to position itself as both a premium and an accessible product.

Branding plays a key role. Olipop uses nostalgic packaging and classic soda flavors. This creates familiarity while communicating a modern health-focused value proposition. The result is strong repeat purchase behavior and brand loyalty.

Olipop Founders

Olipop was founded in 2018 by Ben Goodwin and David Lester. The company was built to rethink traditional soda using a functional, gut-health-focused approach. Both founders brought prior experience in beverage innovation and nutritional science. Their shared goal was clear. Create a product that delivers the taste of classic soda while improving digestive health.

Ben Goodwin

Ben Goodwin is the co-founder and CEO of Olipop. He leads overall strategy, brand positioning, and product direction.

Before launching Olipop, Goodwin co-founded Obi Probiotic Soda. That experience exposed key gaps in the market. Consumers wanted healthier soda, but they would not compromise on taste. Goodwin used these insights to design Olipop as a better-balanced product.

His expertise lies in consumer behavior and brand building. He focuses on making functional beverages feel mainstream rather than niche.

David Lester

David Lester is the co-founder responsible for formulation and product science.

He has a background in nutrition, herbal medicine, and digestive health research. At Olipop, he developed the core formulation using prebiotics, plant fibers, and botanicals.

Lester ensures that every product delivers functional benefits without sacrificing flavor. His role is critical in maintaining product credibility and differentiation in a crowded beverage market.

How the Founders Work Together

Goodwin and Lester operate with a complementary structure. Goodwin drives brand and growth strategy. Lester focuses on product integrity and innovation.

A practical example is Olipop’s Classic Cola. Goodwin ensured it matches the taste expectations of traditional soda drinkers. Lester engineered the formulation to include gut-friendly ingredients. This collaboration defines Olipop’s product success.

Ownership History

The ownership history of Olipop follows a typical high-growth startup trajectory. It began as a founder-controlled company and evolved into a venture-backed business with multiple institutional stakeholders. Each funding stage reshaped equity distribution, governance, and strategic direction.

Founder-Owned Phase (2018–Early Stage)

At launch in 2018, Olipop was fully owned by its founders, Ben Goodwin and David Lester.

During this phase:

- The founders held nearly all equity.

- Decision-making was centralized.

- Product development and early market testing were the primary focus.

This structure allowed rapid experimentation. For example, early formulations and branding decisions were made without external investor pressure. This helped refine the core value proposition before scaling.

Seed and Early Investor Entry

Once initial traction was established, Olipop raised seed funding. This introduced angel investors and early-stage funds into the cap table.

Key changes during this phase:

- Founders diluted a portion of their equity.

- External investors gained minority stakes.

- Informal advisory influence began to shape strategy.

This capital was typically used for:

- Expanding production capacity.

- Improving formulations.

- Securing retail placements.

For example, moving from small-batch production to larger manufacturing runs required upfront capital. Seed funding enabled that transition.

Series A: Institutional Validation

The Series A round marked Olipop’s transition from startup to growth-stage company. Venture capital firms began taking larger positions.

During this stage:

- Institutional investors acquired significant minority stakes.

- A formal board structure started to take shape.

- Governance became more structured.

This round validated Olipop’s business model. It also enabled expansion into major retail chains. At this point, ownership shifted from founder-heavy to a shared structure between founders and investors.

Growth Rounds (Series B and Beyond)

As demand accelerated, Olipop raised additional funding rounds from larger venture firms such as Greenoaks Capital and J.P. Morgan Growth Equity Partners.

Key developments in this phase:

- Institutional investors collectively became majority stakeholders.

- The board of directors expanded to include investor representatives.

- Strategic decisions required broader consensus.

Equity dilution continued, but the company’s valuation increased significantly. This is a standard trade-off in venture-backed scaling.

A practical example is retail expansion. Entering national chains requires inventory financing, logistics, and marketing spend. Growth capital made this possible but came at the cost of reduced founder ownership percentage.

Late-Stage Positioning (Pre-IPO or Acquisition Optionality)

In its current stage, Olipop operates as a late-stage private company.

Ownership characteristics now include:

- Founders retain meaningful but non-majority stakes.

- Venture capital firms hold large combined ownership.

- Smaller investors and strategic partners hold minority positions.

At this point, ownership is structured for flexibility. The company can pursue:

- An initial public offering (IPO).

- Acquisition by a major beverage company.

- Continued private scaling.

Ownership Position as of May 2026

As of May 2026, Olipop operates with a consolidated but distributed ownership structure typical of late-stage private consumer brands.

The founders remain the largest individual shareholders. Their combined stake is substantial, but not controlling on its own. Control is exercised through leadership roles, board influence, and alignment with key investors.

Institutional investors collectively hold the majority of equity. However, ownership is fragmented across multiple funds. No single investor has outright control. This creates a balance of power rather than central dominance.

Early investors and angels are now heavily diluted. Their stakes are financially meaningful but operationally passive. They do not influence day-to-day decisions.

A smaller layer of strategic and celebrity investors exists. These stakeholders hold minor equity positions. Their value is not governance-driven. It is brand-driven, often contributing to visibility, partnerships, and market positioning.

Who Owns Olipop?

![Who Owns Olipop [Infographic]](https://brandsownedby.com/wp-content/uploads/2026/05/Who-Owns-Olipop-Infographic-683x1024.png)

The ownership of Olipop is structured as a late-stage private company with a layered cap table. It combines meaningful founder ownership with concentrated institutional capital and a long tail of smaller investors.

As of May 2026, Olipop is not controlled by a single shareholder. Instead, control is exercised through a combination of equity, board representation, and executive roles. The founders remain the largest individual stakeholders, while venture firms collectively hold the majority of shares.

Based on funding rounds, dilution patterns, and investor participation, the ownership distribution can be realistically interpreted as:

- Founders (combined): 28%–32%.

- Institutional investors (combined): 55%–60%.

- Early investors and angels: 5%–8%.

- Strategic and celebrity investors: 3%–5%.

These ranges reflect private market estimates. Exact figures are not publicly disclosed, but the structure aligns with late-stage venture-backed consumer brands.

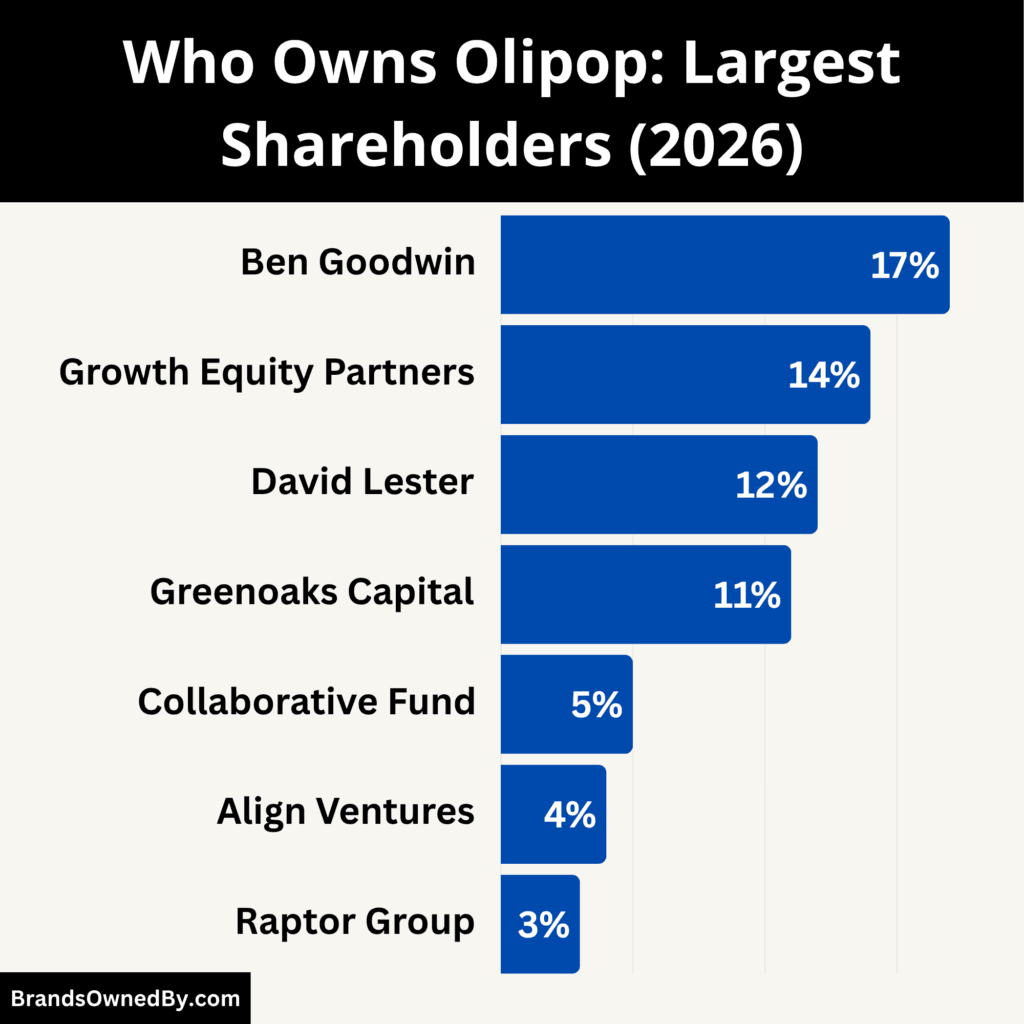

Ben Goodwin (Co-Founder and CEO) — Estimated 16%–18%

Ben Goodwin is the largest individual shareholder.

His ownership has diluted across multiple funding rounds, but he still holds a double-digit stake. More importantly, he holds operational control as CEO.

In practical terms, Goodwin’s influence exceeds his equity percentage. He drives:

- Brand positioning and go-to-market strategy.

- Product roadmap decisions.

- Capital allocation priorities.

For example, Olipop’s decision to prioritize national retail expansion over rapid SKU diversification reflects founder-led strategy rather than investor-driven short-term optimization.

David Lester (Co-Founder) — Estimated 10%–14%

David Lester holds the second-largest individual stake.

His ownership is slightly lower than Goodwin due to role structure and dilution differences. However, it remains substantial.

Lester’s influence is concentrated in product and formulation. His equity aligns with long-term product integrity rather than short-term scaling pressure.

Together, Goodwin and Lester form the single largest ownership block, even though they do not hold a majority.

J.P. Morgan Growth Equity Partners — Estimated 12%–15%

J.P. Morgan Growth Equity Partners is one of the most influential institutional shareholders.

The firm led the latest major funding round and likely secured a double-digit stake. Its ownership places it among the top external shareholders.

Its role includes:

- Board-level participation.

- Oversight on capital efficiency.

- Strategic input on exit pathways such as IPO or acquisition.

Unlike founders, its influence is exercised through governance rather than operations.

Greenoaks Capital — Estimated 10%–12%

Greenoaks Capital is another major institutional investor with a significant stake.

Greenoaks typically builds concentrated positions in high-growth companies. Its estimated ownership places it close to J.P. Morgan in influence.

The firm focuses on long-term value creation. It supports scaling decisions such as:

- Supply chain expansion.

- Retail penetration.

- International growth readiness.

Collaborative Fund — Estimated 4%–6%

Collaborative Fund entered early in Olipop’s lifecycle.

As an early investor, it acquired equity at a lower valuation. However, its stake has been diluted through later rounds.

Despite this, it remains a meaningful shareholder. Its influence is strategic rather than controlling, often aligned with brand and mission consistency.

Align Ventures — Estimated 3%–5%

Align Ventures holds a mid-tier minority stake.

The firm focuses on consumer and wellness brands. Its investment supports Olipop’s positioning within the functional beverage category.

Its ownership does not translate into control but contributes to the broader institutional majority.

Raptor Group — Estimated 2%–4%

Raptor Group is part of the extended institutional base.

Its stake is smaller compared to lead investors. However, it contributes to the overall investor block that collectively holds majority ownership.

Its role is primarily financial, with limited operational involvement.

Other Institutional Investors — Estimated 8%–12% Combined

This category includes multiple funds such as Clerisy and other late-stage participants.

Individually, each holds a small stake. Collectively, they form a meaningful ownership layer.

Their characteristics:

- Limited individual control.

- Participation in funding rounds.

- Indirect influence through board alignment.

This group strengthens the company’s capital base without concentrating power.

Early Investors and Angels — Estimated 5%–8% Combined

Seed investors now hold diluted positions.

While their percentage ownership has decreased, their returns have increased significantly due to valuation growth.

They are largely passive stakeholders with minimal governance influence.

Celebrity and Strategic Investors — Estimated 3%–5% Combined

Olipop has attracted high-profile investors, including:

- Gwyneth Paltrow.

- Mindy Kaling.

- Jonas Brothers.

Each holds a small equity stake, typically below 1% individually.

Their importance is strategic:

- Brand amplification.

- Consumer trust building.

- Cultural positioning.

For example, celebrity involvement has helped Olipop expand awareness beyond traditional health-conscious consumers into mainstream audiences.

Competitor Ownership Comparison

Ownership structure directly shapes how beverage companies scale, make decisions, and compete. When you compare Olipop with its closest competitors, the differences are structural rather than superficial. Olipop operates as a founder-led, venture-backed company. Most competitors fall into either publicly traded corporations or strategically controlled brands.

| Company | Ownership Type | Largest Shareholder(s) | Approx. Stake of Largest Shareholder | Control Model | Practical Impact on Strategy |

|---|---|---|---|---|---|

| Olipop | Private (Venture-Backed) | Founders + institutional investors (e.g., J.P. Morgan Growth Equity Partners) | No single majority (largest individual ~17%) | Founder-led with investor board oversight | Fast decision-making, high flexibility, independent brand strategy |

| The Coca-Cola Company | Public | Berkshire Hathaway | ~9% | Board-driven, executive-led | Highly structured decisions, slower execution due to global scale |

| PepsiCo | Public | The Vanguard Group, BlackRock | ~7%–8% each | Board and executive management | Stable governance, but slower pivots due to portfolio complexity |

| Poppi | Private (Strategic-Backed) | Founders + PepsiCo | Minority but strategic stake | Hybrid (founder + corporate influence) | Faster scaling via PepsiCo distribution, reduced strategic independence |

| Keurig Dr Pepper | Public (Strategic Influence) | JAB Holding Company | ~30% | Strategic investor + board governance | Strong financial backing, but strategy aligned with major shareholder |

Olipop vs Coca-Cola

The Coca-Cola Company represents a fully mature public ownership model. Its shares are widely held, but a few large institutions dominate voting power. Berkshire Hathaway is the largest long-term shareholder, holding roughly 9% of the company. Other major stakes sit with passive asset managers like Vanguard and BlackRock.

Despite this distributed ownership, control is highly structured. Strategic decisions are driven by executive leadership and approved by a formal board. Individual shareholders do not influence operations directly.

Olipop operates very differently. It is privately held, and its ownership is concentrated among founders and a small group of investors. Decision-making is faster because it does not require public shareholder alignment.

For example, launching a new product line at Olipop can move from concept to retail much quicker than at Coca-Cola, where multiple internal approvals and global coordination are required.

Olipop vs PepsiCo

PepsiCo follows a similar public structure. Its largest shareholders, including The Vanguard Group and BlackRock, each hold around 7%–8%.

Ownership is stable and long-term. However, it is also passive. These institutions influence governance through voting but do not shape daily operations.

The key difference is control speed and flexibility. PepsiCo operates across hundreds of brands and global markets. Any strategic shift must align with a broader portfolio. Olipop, in contrast, is focused on a single category. Its ownership structure allows it to prioritize category disruption without internal competition for resources.

A practical example is functional soda expansion. Olipop can allocate capital entirely to this niche. PepsiCo must balance it against legacy brands like Pepsi and Mountain Dew.

Olipop vs Poppi

Poppi is the closest structural comparison to Olipop, but with a critical difference. Poppi has taken strategic investment from PepsiCo.

This changes how ownership translates into control. PepsiCo does not necessarily own a majority stake, but its involvement brings distribution power, supply chain advantages, and strategic influence.

Poppi benefits from this backing. It can scale faster in retail and leverage PepsiCo’s infrastructure. However, it also operates within PepsiCo’s broader strategic framework. Product decisions, pricing, and expansion are influenced by corporate priorities.

Olipop has chosen to remain independent. This gives it full control over brand positioning and product innovation. The trade-off is that it must build distribution and operations without a large corporate partner.

Olipop vs Keurig Dr Pepper

Keurig Dr Pepper sits between public and controlled ownership. It is publicly listed, but JAB Holding Company holds a major stake of roughly 30%.

This creates a semi-concentrated ownership model. JAB has significant influence over long-term strategy, acquisitions, and capital allocation.

Compared to Olipop, this structure reduces independence. Strategic decisions are aligned with JAB’s broader portfolio, which includes multiple beverage and consumer brands.

Olipop does not have a dominant shareholder like JAB. Its ownership is more balanced. No single investor can dictate direction, which keeps founders in control of strategy.

What This Means in Practice

The ownership differences translate into real operational outcomes.

Olipop can test new flavors, reposition branding, or enter new channels quickly because decisions are centralized among founders and a small board.

Coca-Cola and PepsiCo move at scale but with slower execution cycles. Their ownership structure prioritizes stability over speed.

Poppi scales faster than Olipop due to corporate backing but sacrifices some independence.

Keurig Dr Pepper benefits from strong financial backing but operates within the strategic boundaries set by a major shareholder.

Who Controls Olipop?

Control at Olipop is not concentrated in a single shareholder. It is structured across founders, board governance, and investor rights. As of May 2026, the company operates under a founder-led but board-constrained model, which is typical for late-stage private companies valued above $1 billion.

Founder Control: Ben Goodwin as Executive Authority

Ben Goodwin is the primary control point inside the company. He has been CEO since 2018 and has never been replaced or supplemented by an external operator. This matters because, in venture-backed companies, leadership transitions are often the point where founders lose control. That has not happened at Olipop.

Goodwin’s control is operational and strategic. He is responsible for defining category positioning, which in Olipop’s case is the “functional soda” segment. This is not a marketing label. It determines pricing, distribution strategy, and competitive positioning against both traditional soda and health beverages.

His authority extends to execution. Decisions around retail expansion, SKU prioritization, and brand direction are made internally under his leadership. Investors do not participate in these decisions unless they involve capital risk. This separation keeps execution centralized and fast.

Product Control: David Lester and Internal IP Ownership

David Lester controls the formulation layer, which is the core intellectual property of Olipop. This is a critical control point because the company’s differentiation is not branding alone. It is based on its ingredient system and digestive health positioning.

Lester’s role ensures that product decisions are not influenced by external investors or contract manufacturers. The formulations are developed and controlled internally. This prevents dilution of product quality, which is a common issue when companies scale rapidly under investor pressure.

In practical terms, this creates a dual-control system. Goodwin controls commercial execution. Lester controls product integrity. Neither function is outsourced or investor-driven, which keeps the core business aligned.

Board Governance: Where Founder Control Has Limits

Control shifts when decisions move beyond operations into capital allocation or structural changes. This is where the board becomes the controlling authority.

After the 2025 Series C round led by J.P. Morgan Growth Equity Partners, the board includes both founders and investor representatives. This is not symbolic. Board composition determines who can approve or block major decisions.

The board has authority over:

- New funding rounds and dilution events.

- Large capital expenditures such as manufacturing expansion.

- Exit decisions, including acquisition or IPO.

This means Goodwin cannot independently raise capital or sell the company. Those actions require board approval, where investors have voting power.

However, the board does not interfere in day-to-day operations. It operates at the level of financial oversight and long-term direction, not execution.

Investor Control: Collective Power Without Dominance

Institutional investors, including Greenoaks Capital and J.P. Morgan Growth Equity Partners, collectively hold the majority of equity. Despite this, control is not centralized.

No single investor holds a controlling stake. The largest individual investor owns a mid-teens percentage. This prevents unilateral control by any one firm.

Investor influence is exercised through:

- Board seats and voting rights.

- Approval or rejection of major financial decisions.

- Influence over long-term strategic direction.

This creates a system where investors can block decisions but cannot independently run the company. They depend on alignment with founders to move forward.

Leadership Stability and Its Impact on Control

Olipop has had a single CEO since its founding in 2018. There has been no transition to a professional CEO, no interim leadership phase, and no restructuring of executive authority. This is a critical detail because, in venture-backed companies, control often shifts when investors install external leadership during growth stages.

That transition typically redistributes power away from founders. It introduces a more investor-aligned execution model, often prioritizing short-term scaling efficiency over founder vision. Olipop has avoided this shift entirely.

Because Ben Goodwin has remained CEO throughout all funding rounds, control has stayed internally consistent. Strategic direction, brand positioning, and execution philosophy have not been reset or diluted across leadership changes. This continuity ensures that investor influence remains at the governance level rather than operational control.

It also signals investor confidence. Maintaining a founder as CEO at a ~$1.8B valuation implies that investors are aligned with existing leadership rather than seeking to replace it.

How Control Functions in Real Decisions

Control becomes clearer when mapped to actual decisions.

If Olipop launches a new flavor, that decision is made entirely at the founder level. It does not require investor approval because it does not materially impact capital structure.

If Olipop decides to build a new production facility, the process changes. The founders define the strategy, but the board must approve the capital allocation. Investors evaluate the financial risk before approving.

If Olipop considers an acquisition offer, control shifts further. The board, representing shareholder interests, becomes the final decision-making authority. Founders can influence the outcome, but they cannot approve or reject it unilaterally.

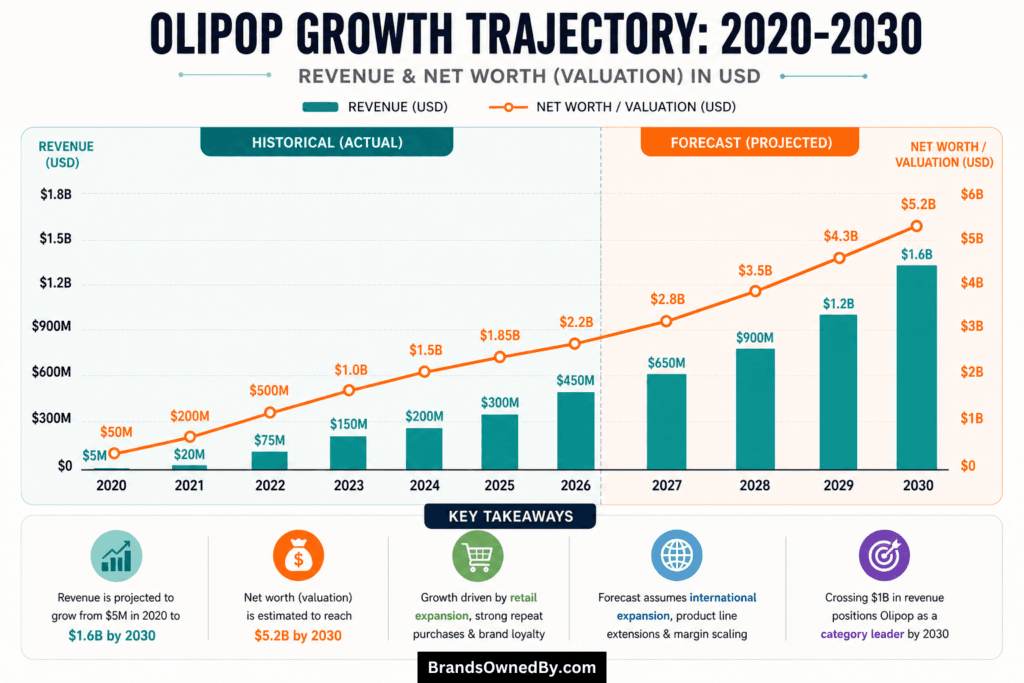

Olipop Annual Revenue and Net Worth

As of May 2026, the company is estimated to generate around $450 million in annual revenue with a net worth (valuation) of approximately $2.2 billion. This places Olipop firmly in the late-stage growth category, competing directly with established beverage brands in terms of scale, not just positioning.

2026 Revenue

The $450 million revenue is not evenly distributed. It is concentrated across key retail channels:

- Mass Retail (Target, Kroger, Walmart): 55% ($247 million)

This is the largest contributor. These retailers drive volume through national distribution and high foot traffic. Growth here is driven by increased shelf facings and strong weekly sales velocity. - Natural & Specialty Retail (Whole Foods, Sprouts): 25% ($112 million)

This channel delivers higher per-unit margins and strong brand loyalty. It also acts as a testing ground for new SKUs before scaling into mass retail. - Convenience & Emerging Channels: 10% ($45 million)

Includes smaller retail formats and convenience stores. This is still underpenetrated but growing, especially for impulse purchases. - E-commerce & Direct-to-Consumer: 10% ($45 million)

Includes online platforms and subscriptions. This channel has higher margins but lower volume compared to retail.

This breakdown shows that Olipop’s revenue is heavily dependent on mass retail scale, while premium channels support margins and brand positioning.

Revenue Bifurcation (Product-Level)

Revenue concentration is also visible at the SKU level:

- Core Flavors (Vintage Cola, Root Beer, Orange Squeeze): 60% ($270 million)

These are high-velocity SKUs with consistent repeat demand. - Secondary Flavors (Strawberry Vanilla, Cherry Cola, Grape): 30% ($135 million)

These drive incremental sales and help expand shelf presence. - Seasonal / Limited Editions: 10% ($45 million)

These create spikes in demand but are not core revenue drivers.

This concentration improves operational efficiency. Manufacturing and supply chains can focus on fewer high-performing SKUs.

Revenue Bifurcation (Geographic)

Olipop’s revenue is still heavily U.S.-centric:

- United States: 95% ($427 million)

- International (early-stage markets): 5% ($23 million)

International markets are not yet a major contributor but represent future growth potential.

At $450 million revenue, Olipop is operating with improving unit economics:

- Gross margin estimate: 45%–50%

Driven by premium pricing and scaling production. - Retail margins: Lower in mass retail, higher in specialty channels.

- Customer acquisition cost: Declining due to strong repeat purchase rates.

This margin profile supports the current valuation and indicates movement toward profitability.

2026 Net Worth

The estimated $2.2 billion valuation reflects a shift in how investors view Olipop. At earlier stages, valuation was driven primarily by growth potential. In 2026, it is driven by execution quality and scalability.

At $450 million in revenue, the implied valuation multiple is roughly 4.8x–5x revenue. This multiple is consistent with late-stage consumer brands that have demonstrated:

- Strong retail performance across national chains.

- High repeat purchase rates.

- Improving gross margins due to scale.

Investors are now pricing Olipop as a durable brand rather than a speculative growth play. The company’s ability to maintain premium pricing while scaling volume is a key factor in this valuation.

Another important factor is category positioning. Olipop is not competing only within traditional soda. It operates in the functional beverage segment, which is growing faster than the broader soft drink market. This gives it a structural advantage that supports higher valuation multiples.

Revenue Forecast (2027–2030)

The projected growth is based on distribution density, international rollout, and SKU expansion. Below is a more structured breakdown of how revenue scales:

- 2027: $650 million

Growth is primarily driven by deeper penetration in existing U.S. retailers. Shelf facings increase, and velocity improves. Convenience channel expansion begins contributing meaningfully. - 2028: $900 million

International markets begin scaling, contributing ~10%–12% of revenue. New product formats (e.g., multi-packs, adjacent functional beverages) increase average basket size. - 2029: $1.2 billion

Olipop crosses into billion-dollar brand territory. Revenue diversification improves, with international markets contributing ~15%–18%. Supply chain efficiencies improve margins further. - 2030: $1.6 billion

The company operates at near full-scale distribution across North America and selected international markets. Revenue growth is driven more by market share gains than new market entry.

The 2026 structure shows a company that is no longer experimenting. It is optimizing.

Revenue is concentrated, predictable, and driven by repeat consumption. Growth is no longer dependent on new distribution alone but on increasing productivity within existing channels.

The forecast reflects a transition from rapid expansion to scaled execution, where gains come from efficiency, international growth, and category leadership rather than pure discovery.

Brands Owned by Olipop

As of 2026, it follows a single-brand, multi-product strategy. Unlike large beverage corporations that acquire and manage multiple brands, Olipop has deliberately avoided acquisitions and mergers. Its focus is on building depth within one brand rather than expanding breadth across multiple entities.

That said, within this single-brand structure, Olipop operates multiple product lines, formulations, and internal brand extensions that function as distinct revenue drivers.

Olipop Core Brand

The Olipop brand itself is the primary and only major commercial entity.

It is positioned as a functional soda brand, not a traditional beverage label. This distinction is important. The company does not market itself as a soft drink company. Instead, it competes in the intersection of soda, wellness beverages, and digestive health products.

The brand operates across:

- National retail distribution (Target, Kroger, Whole Foods).

- Direct-to-consumer channels.

- Emerging convenience retail formats.

All revenue flows through this single brand, making it the central asset of the company.

Olipop Classic Soda Line

This is the largest and most commercially important product line under the Olipop brand.

It includes flavors designed to replicate traditional soda experiences:

- Vintage Cola.

- Root Beer.

- Orange Squeeze.

These products generate the majority of revenue. They are engineered to match the taste profile of legacy sodas while incorporating prebiotic fiber and botanical ingredients.

From an operational standpoint, this line drives:

- High retail velocity.

- Strong repeat purchase rates.

- Consistent shelf placement in mass retail.

This is effectively the core revenue engine of the company.

Olipop Functional Flavor Extensions

Beyond classic soda replication, Olipop has developed a range of secondary flavors that expand its market reach.

These include:

- Strawberry Vanilla.

- Cherry Cola.

- Grape.

- Lemon Lime.

These products serve two purposes.

First, they increase shelf presence. Retailers allocate more space to brands with a wider SKU range. Second, they attract different consumer segments who may not prefer traditional cola-style beverages.

While these flavors generate less revenue individually compared to core SKUs, collectively they contribute a significant share of total sales.

Olipop Limited Edition and Seasonal Releases

Olipop regularly launches limited-time flavors and seasonal variants.

These are not permanent SKUs. They are used strategically to:

- Test new formulations.

- Drive short-term demand spikes.

- Maintain consumer engagement.

Examples include seasonal flavors tied to summer or holiday periods.

From a business perspective, these releases function as market testing tools. Successful limited editions can be converted into permanent SKUs if they demonstrate strong retail performance.

Olipop Functional Formulation Platform

Internally, Olipop operates a proprietary formulation system based on prebiotics, plant fibers, and botanicals.

This is not marketed as a separate brand, but it functions as a core internal asset.

The formulation platform includes ingredients such as:

- Cassava root fiber.

- Chicory root.

- Marshmallow root.

This system is what differentiates Olipop from traditional soda companies. It allows the brand to claim functional health benefits while maintaining taste.

From a strategic perspective, this platform is equivalent to intellectual property. It underpins all products and enables future expansion into adjacent categories.

Direct-to-Consumer and Subscription Channel

Olipop also operates its own direct-to-consumer ecosystem.

While not a separate brand, this channel functions as an internal business unit with distinct economics.

Key characteristics include:

- Higher margins compared to retail.

- Subscription-based recurring revenue.

- Direct access to customer data.

This channel allows Olipop to test new products quickly and gather feedback before scaling into retail.

Conclusion

If you are analyzing who owns Olipop, the answer reflects a modern startup structure. The company is owned by its founders and a group of venture capital investors. No large beverage corporation controls it.

This independence is a strategic advantage. It allows Olipop to compete directly with legacy soda giants while maintaining a health-first identity. However, as competition intensifies, future ownership changes or acquisitions remain a realistic possibility.

FAQs

Who manufactures Olipop?

Olipop does not rely on a single in-house manufacturing facility. Production is handled through a network of contract manufacturers (co-packers) across the United States.

These partners are responsible for large-scale production, bottling, and distribution logistics. Olipop controls the formulation, ingredient sourcing, and quality standards, while manufacturing is outsourced for scalability. This model allows the company to expand quickly without heavy capital investment in factories.

Who is Olipop owned by?

Olipop is a privately owned company.

Ownership is split between its founders, Ben Goodwin and David Lester, and a group of institutional investors such as J.P. Morgan Growth Equity Partners and Greenoaks Capital.

Founders are the largest individual shareholders, while investors collectively hold the majority stake. No single company owns Olipop outright.

Who makes Olipop?

Olipop is developed and produced under the direction of its founders and internal team.

- Product formulation is led by David Lester.

- Brand and business operations are led by Ben Goodwin.

The actual manufacturing is carried out by third-party co-packers, but the recipe, ingredients, and quality control are fully owned and managed by Olipop.

Is OLIPOP actually healthy?

Olipop is positioned as a healthier alternative to traditional soda, but it should not be treated as a health supplement.

Compared to regular soda, it offers:

- Much lower sugar content.

- Added prebiotic fiber (typically 6–9 grams per can).

- Plant-based ingredients aimed at supporting gut health.

However, it is still a flavored beverage. While it is significantly better than conventional sugary sodas, it is not equivalent to whole foods or essential nutrition sources.

In practical terms, Olipop is a “better-for-you soda,” not a health product.

What is the #1 healthiest soda?

There is no single universally recognized “#1 healthiest soda,” because health depends on individual dietary needs.

However, in the functional soda category, brands like:

- Olipop

- Poppi

are often considered among the healthiest options available.

They stand out because they:

- Contain significantly less sugar than traditional sodas.

- Include functional ingredients like prebiotics.

- Avoid high-fructose corn syrup.

That said, the healthiest choice overall is still water or unsweetened beverages. Functional sodas are simply a better alternative within the soda category, not a replacement for healthy drinks entirely.