- Capital One is a publicly traded company listed on the NYSE (COF) and is owned by shareholders rather than a private individual or parent company.

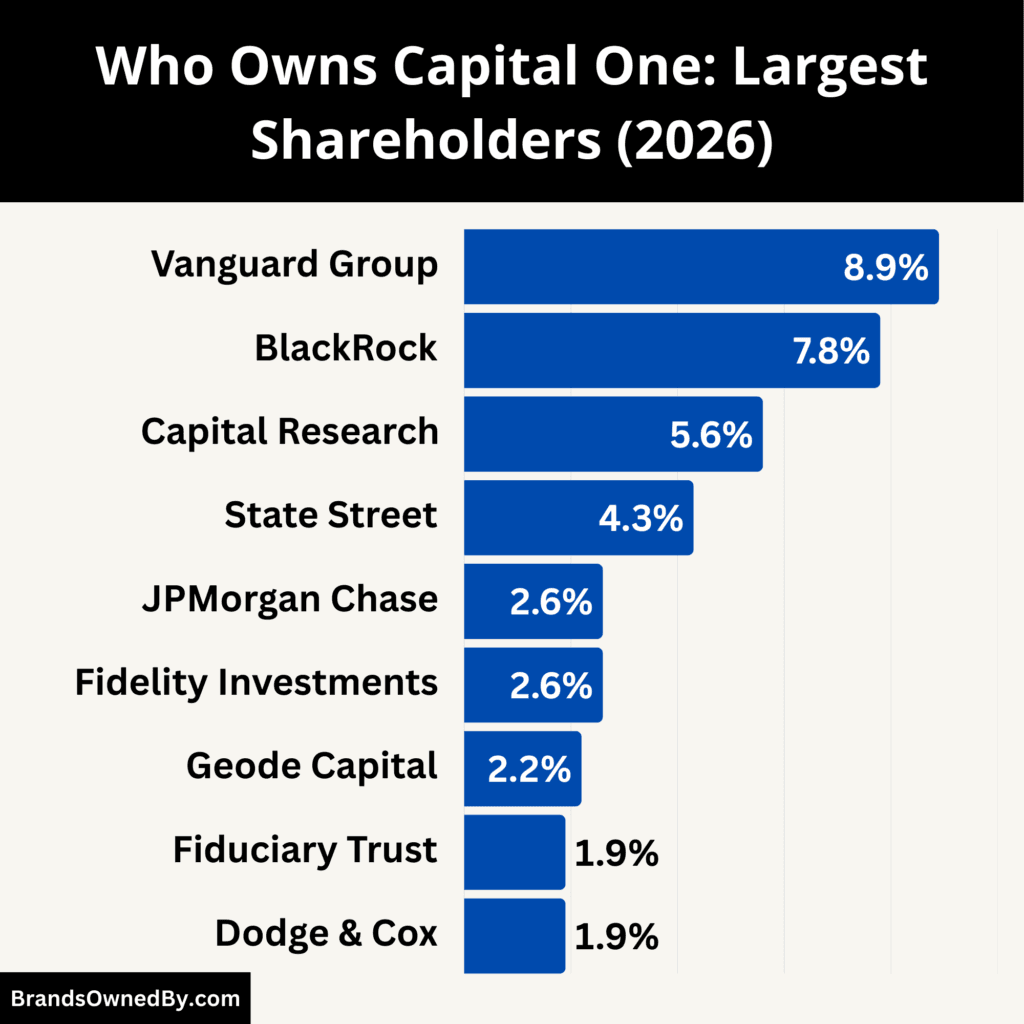

- The largest shareholders are institutional investors, led by The Vanguard Group (8.9%), BlackRock (7.8%), Capital Research and Management Company (5.6%), and State Street Corporation (4.3%) as of 2026.

- No single shareholder owns a controlling stake. The top institutional investors collectively hold a significant portion of shares, but none individually exceeds 10%.

- Operational control is separate from ownership, with CEO Richard D. Fairbank leading the company under board oversight while shareholders exercise influence through voting rights.

Capital One Financial Corporation is a diversified bank holding company headquartered in McLean. It operates as a full-service financial institution with a strong national footprint in consumer banking, credit cards, auto lending, and commercial banking.

The company is structured as a bank holding company regulated under U.S. federal banking laws. It provides services primarily in the United States, with selected international credit card operations. Capital One is widely recognized for its data-driven underwriting model and technology-first approach to banking.

Its brand is built around digital innovation, customer analytics, and direct-to-consumer financial products. Over the years, it has evolved from a monoline credit card issuer into a diversified national bank.

Capital One operates through four main segments: credit cards, consumer banking, commercial banking, and auto finance.

Its credit card business is one of the largest in the United States. The consumer banking division offers checking, savings, and branch-based services, including Capital One Cafés. The commercial segment serves middle-market and corporate clients. Auto finance provides lending solutions through dealerships and direct channels.

The company emphasizes technology and analytics. It uses data modeling to manage risk, personalize offers, and improve customer experience.

Founders of Capital One

Richard D. Fairbank and Nigel Morris founded Capital One in 1994 after it was spun off from Signet Financial.

Richard Fairbank, who remains Chairman and CEO, shaped the company’s analytical lending strategy. He introduced a test-and-learn model that customized credit products using customer data.

Nigel Morris served as an early executive and helped build the company’s operational and analytics systems. Although he later left the company, his role was central during its formative years.

From the beginning, Capital One focused on data-driven decision making. Instead of offering uniform products, it tailored credit terms based on customer behavior.

This analytical approach allowed the company to scale quickly and compete with larger banks. The same technology-led strategy continues to define Capital One today.

Ownership History

Capital One Financial Corporation has operated under a public ownership model since its formation as an independent company. Its ownership structure has always been tied to public equity markets rather than private family control or state ownership.

Spin-Off from Signet Financial (1994)

Capital One was created in 1994 as a spin-off from Signet Financial Corp, a regional bank based in Virginia. Before the spin-off, the credit card division operated within Signet.

When Capital One became independent, shares were distributed to existing Signet shareholders. From that point onward, the company functioned as a standalone, publicly traded corporation. Ownership shifted from a parent bank structure to a dispersed shareholder base.

This marked the beginning of Capital One’s modern ownership history.

Early Public Market Expansion

After becoming publicly listed on the New York Stock Exchange under the ticker COF, Capital One attracted institutional investors. Mutual funds, pension funds, and asset managers began acquiring significant stakes.

During the late 1990s and early 2000s, the company’s rapid growth in credit cards increased investor interest. Ownership became increasingly concentrated in large institutional portfolios. However, no single shareholder gained majority control.

Insiders, including founders and executives, retained equity stakes. These holdings were meaningful but not controlling.

Acquisition Phase and Shareholder Diversification

Between 2005 and 2012, Capital One completed major acquisitions that expanded its scale in retail and digital banking. Notable deals included Hibernia National Bank and ING Direct USA.

These transactions were financed through combinations of stock and cash. As new shares were issued, the shareholder base broadened. Institutional ownership increased further due to index fund inclusion and growing market capitalization.

During this period, Capital One’s ownership profile began to resemble other large U.S. bank holding companies. The majority of shares were held by institutional investors managing funds on behalf of retail clients.

Rise of Passive Institutional Ownership

In the 2010s and 2020s, passive investment strategies gained dominance in U.S. equity markets. Large asset managers such as The Vanguard Group, BlackRock, and State Street Corporation became the largest shareholders of Capital One.

These firms typically hold shares through index funds and exchange-traded funds. They do not actively manage daily operations. Instead, they vote on corporate governance matters and board elections.

This shift increased the proportion of institutional ownership while reducing the relative impact of smaller individual shareholders.

Current Ownership Structure as of 2026

As of 2026, Capital One’s ownership remains widely dispersed. The majority of outstanding shares are held by institutional investors. Retail investors and insiders hold smaller percentages.

No individual or entity owns a controlling stake. The founders do not maintain majority ownership. Control is therefore separated from ownership.

This structure aligns with governance norms among major U.S. banks. Shareholders elect the board of directors. The board appoints executive leadership. Strategic decisions are guided by management within the framework set by regulators and corporate governance standards.

In summary, Capital One’s ownership history reflects a transition from a bank division within Signet to a fully independent, publicly owned financial institution with diversified institutional shareholders and no controlling owner.

Who Owns Capital One: Top Shareholders

Capital One is a publicly traded company listed on the New York Stock Exchange under the ticker COF.

As of 2026, the largest shareholder is The Vanguard Group, followed by BlackRock and other major institutional asset managers. Most of Capital One’s shares are held by institutional investors through mutual funds, ETFs, pension funds, and investment portfolios. No single shareholder owns a controlling stake. Governance is exercised through shareholder voting, board oversight, and executive leadership.

The Vanguard Group

The Vanguard Group is the largest shareholder of Capital One, holding approximately 8.9% of the company’s outstanding shares as of 2026.

Vanguard’s stake is primarily held through index funds and exchange-traded funds that track major U.S. equity indices. These funds include total market funds and financial sector ETFs. Vanguard does not directly manage Capital One’s operations. However, due to its large ownership position, it plays an important role in corporate governance.

Vanguard votes on key matters such as board elections, executive compensation policies, and shareholder proposals. Its investment approach is long-term and passive. This means it typically maintains its position rather than frequently trading shares.

BlackRock

BlackRock is the second-largest shareholder, owning approximately 7.8% of Capital One as of 2026.

BlackRock’s shares are held through its iShares ETFs, institutional accounts, and actively managed funds. Like Vanguard, BlackRock invests on behalf of millions of clients, including pension funds, governments, and individual investors.

Through its stewardship team, BlackRock engages with company leadership on governance, risk oversight, and long-term strategy. While it does not control Capital One, its voting power makes it one of the most influential shareholders.

Capital Research and Management Company

Capital Research and Management Company holds approximately 5.6% of Capital One’s shares.

Capital Research operates under the Capital Group brand and follows an active investment strategy. Unlike passive index funds, it conducts detailed fundamental research before building positions.

Its investment in Capital One reflects a long-term view of the company’s competitive position in credit cards and consumer banking. Because it is an active manager, its ownership is based on conviction rather than automatic index inclusion.

State Street Corporation

State Street Corporation owns approximately 4.3% of Capital One through its asset management division, State Street Global Advisors.

State Street is one of the largest ETF providers globally. Its holdings in Capital One are largely tied to index-tracking strategies. Similar to Vanguard and BlackRock, State Street participates in governance through proxy voting and board engagement.

Although its investment style is primarily passive, its ownership stake gives it measurable influence in shareholder decisions.

JPMorgan Investment Management

JPMorgan Chase, through its asset management arm, holds approximately 2.6% of Capital One’s shares.

This position is spread across diversified mutual funds, retirement products, and institutional portfolios. JPMorgan’s investment strategies include both active and passive approaches.

While it does not have a controlling stake, its ownership contributes to the strong institutional presence in Capital One’s shareholder base.

Fidelity Management & Research

Fidelity Investments, through Fidelity Management & Research Co., owns approximately 2.6% of Capital One.

Fidelity manages a wide range of mutual funds and retirement accounts. Its holdings in Capital One are typically included in diversified large-cap and financial sector funds.

Fidelity’s active management approach means its position is based on internal research and portfolio strategy rather than automatic index replication.

Geode Capital Management

Geode Capital Management holds approximately 2.2% of Capital One.

Geode specializes in quantitative and index-based investment strategies. It often manages assets on behalf of large institutional clients, including pension funds and endowments. Much of its Capital One stake is linked to benchmark replication strategies.

Although Geode does not engage in activist investing, its ownership contributes to the overall concentration of shares among institutional investors. Its presence reflects the dominance of systematic and index-driven capital in modern equity markets.

Fiduciary Trust Company International

Fiduciary Trust Company International owns approximately 1.9% of Capital One.

This firm focuses on wealth management for high-net-worth individuals, families, and charitable foundations. Its stake is typically held within diversified client portfolios rather than sector-specific strategies.

Because Fiduciary Trust manages discretionary accounts, its ownership reflects client-driven asset allocation decisions. While smaller than the largest asset managers, its holdings represent concentrated long-term capital rather than short-term trading positions.

Dodge & Cox

Dodge & Cox holds approximately 1.9% of Capital One.

Dodge & Cox is known for its value-oriented investment philosophy. The firm focuses on companies it considers undervalued relative to fundamentals. Its investment in Capital One signals confidence in the bank’s competitive position and earnings resilience.

Unlike passive index managers, Dodge & Cox conducts independent research and may adjust its holdings based on macroeconomic conditions, credit cycles, and sector outlook. Its involvement reflects active conviction in the company’s long-term prospects.

Insider and Retail Ownership

In addition to institutional shareholders, a portion of Capital One shares is owned by insiders and retail investors.

Richard D. Fairbank, the founder and CEO, holds a personal equity stake. While not large enough to provide control, his ownership aligns leadership interests with shareholder value.

Retail investors collectively own a smaller percentage of outstanding shares. These holdings are typically spread across brokerage accounts and retirement portfolios.

Competitor Ownership Comparison

Capital One’s ownership structure is typical for a large publicly traded U.S. bank. It is widely held, institutionally dominated, and lacks a controlling shareholder. To better understand who owns Capital One, it is useful to compare its shareholder model with other major banking competitors.

| Bank | Publicly Traded | Largest Institutional Shareholders | Founder Involvement | Governance Structure |

|---|---|---|---|---|

| Capital One Financial Corporation | Yes (NYSE: COF) | Vanguard, BlackRock, Capital Research, State Street | Yes – Richard D. Fairbank (Founder & CEO) | Board of Directors + Founder-CEO leadership |

| JPMorgan Chase | Yes (NYSE: JPM) | Vanguard, BlackRock, State Street | No | Board of Directors + Professional CEO |

| Bank of America | Yes (NYSE: BAC) | Vanguard, BlackRock, State Street | No | Board oversight + Executive management |

| Citigroup | Yes (NYSE: C) | Vanguard, BlackRock, State Street | No | Board-elected executive leadership |

JPMorgan Chase Ownership Structure

JPMorgan Chase operates under a similar ownership framework. It is publicly listed and widely held by institutional investors. The largest shareholders are major asset managers such as The Vanguard Group, BlackRock, and State Street Corporation.

No single investor owns a majority stake in JPMorgan Chase. Control is exercised through its board of directors and executive leadership. Institutional investors influence governance through proxy voting, not operational control. The structure closely mirrors Capital One’s model, though JPMorgan’s global scale results in broader institutional exposure across international funds.

Bank of America Ownership Structure

Bank of America also follows a dispersed institutional ownership structure. It is publicly traded and heavily owned by asset management firms. Vanguard and BlackRock rank among its largest shareholders.

There is no family ownership and no dominant controlling investor. Ownership is spread across mutual funds, ETFs, pension funds, and retail investors. Institutional investors collectively hold significant voting power, just as they do in Capital One.

The key difference lies in business diversification. Bank of America’s larger global footprint attracts a wider range of international institutional investors. However, the fundamental ownership structure remains comparable.

Citigroup Ownership Structure

Citigroup operates under the same public shareholder model. It is listed on the New York Stock Exchange and is primarily owned by institutional investors.

Following its post-financial crisis restructuring, Citigroup’s ownership became fully market-driven with no government majority stake. Today, large asset managers dominate its shareholder base. As with Capital One, no single entity controls the company.

Governance is managed through board oversight and executive leadership, while shareholders influence decisions through voting mechanisms.

Key Similarities Across Major U.S. Banks

When comparing Capital One to JPMorgan Chase, Bank of America, and Citigroup, several patterns emerge:

Institutional Dominance: Large asset managers such as Vanguard, BlackRock, and State Street consistently appear as top shareholders across all major U.S. banks.

No Controlling Shareholder: None of these banks has a majority owner. Control is separated from ownership. Strategic decisions are made by management and overseen by boards elected by shareholders.

Passive Investment Influence: Index funds and ETFs hold significant stakes. These investors rarely intervene operationally but influence governance through proxy voting.

Public Market Accountability: All are listed on major stock exchanges. This subjects them to regulatory oversight, earnings transparency, and shareholder activism risk.

Key Differences Between Capital One and Its Competitors

While the ownership structure is broadly similar, there are subtle differences:

Scale of Institutional Ownership: Larger banks such as JPMorgan Chase and Bank of America typically have even higher absolute institutional holdings due to their inclusion in more global index funds.

Business Model Exposure: Capital One has a stronger concentration in credit cards and consumer lending compared to JPMorgan, which has a more diversified global investment banking presence. This can affect the type of funds that invest in each institution.

Insider Ownership: Capital One’s founder, Richard D. Fairbank, maintains a visible insider stake due to his long tenure. This founder-led structure is less common among larger competitors, where leadership turnover has been more frequent.

Who Controls Capital One?

Capital One Financial Corporation is controlled by its executive leadership and board of directors, not by a single owner. It is a publicly traded company with no majority shareholder.

As of 2026, operational control rests with founder, Chairman, and CEO Richard D. Fairbank, while strategic oversight is exercised by the board of directors elected by shareholders. Institutional investors influence governance through voting rights but do not manage daily operations.

Richard D. Fairbank – Chairman and Chief Executive Officer

Richard D. Fairbank serves as both Chairman of the Board and Chief Executive Officer. He has led the company since its formation and remains the primary decision-maker in corporate strategy.

As CEO, Fairbank oversees capital allocation, risk management, technology investment, credit strategy, regulatory positioning, and long-term business planning. Major initiatives, including digital banking expansion, cloud infrastructure investments, and credit portfolio strategy, fall under his authority.

Because he also serves as Chairman, he has significant influence over board agendas and corporate governance priorities. However, he does not hold a controlling equity stake. His authority comes from his executive role and board position rather than ownership concentration.

Board of Directors

Capital One’s board of directors is responsible for oversight and governance. Directors are elected by shareholders during annual meetings. The board is composed primarily of independent directors, which aligns with U.S. corporate governance standards for large bank holding companies.

The board approves major corporate actions, including acquisitions, share repurchase programs, dividend policy, executive compensation, and long-term strategic plans. It also oversees enterprise risk management, regulatory compliance, cybersecurity governance, and capital adequacy frameworks.

Board committees play a central role in control. These include audit, risk, compensation, and governance committees. Each committee provides structured oversight in its respective area. For example, the risk committee monitors credit exposure, liquidity management, and stress testing compliance.

Although large institutional investors such as The Vanguard Group and BlackRock hold significant voting power, they do not participate in board management. Their influence is exercised through proxy voting and engagement on governance matters.

Executive Leadership Structure

Control of day-to-day operations is executed by Capital One’s senior leadership team under the CEO.

The company operates through defined business segments including credit cards, consumer banking, commercial banking, and auto finance. Each segment is led by senior executives responsible for performance, regulatory compliance, operational risk, and profitability.

The Chief Financial Officer oversees capital planning, liquidity management, and financial reporting. The Chief Risk Officer manages credit risk, market risk, operational risk, and regulatory stress testing. Technology leadership oversees cloud infrastructure, cybersecurity, and data analytics platforms, which are central to Capital One’s business model.

This centralized but segmented leadership model ensures operational control is distributed across functional experts while strategic authority remains with the CEO.

Regulatory Oversight and External Constraints

As one of the largest U.S. bank holding companies, Capital One operates under strict supervision from federal regulators. These include the Federal Reserve and the Office of the Comptroller of the Currency.

Regulatory oversight affects capital ratios, stress testing results, dividend approvals, and merger activity. While regulators do not manage the company, their authority significantly shapes risk tolerance and capital allocation decisions.

This regulatory framework acts as an external control mechanism alongside internal governance.

Separation of Ownership and Control

Capital One demonstrates a clear separation between ownership and operational control. Shareholders own the company through publicly traded shares. Institutional investors collectively hold the majority of stock. However, none holds a controlling interest.

Control flows through a governance structure where shareholders elect the board, the board appoints executive leadership, and management runs the company.

As of 2026, effective control of Capital One lies with its executive leadership team led by Richard D. Fairbank, subject to oversight from the board of directors and federal banking regulators.

Capital One Annual Revenue and Net Worth

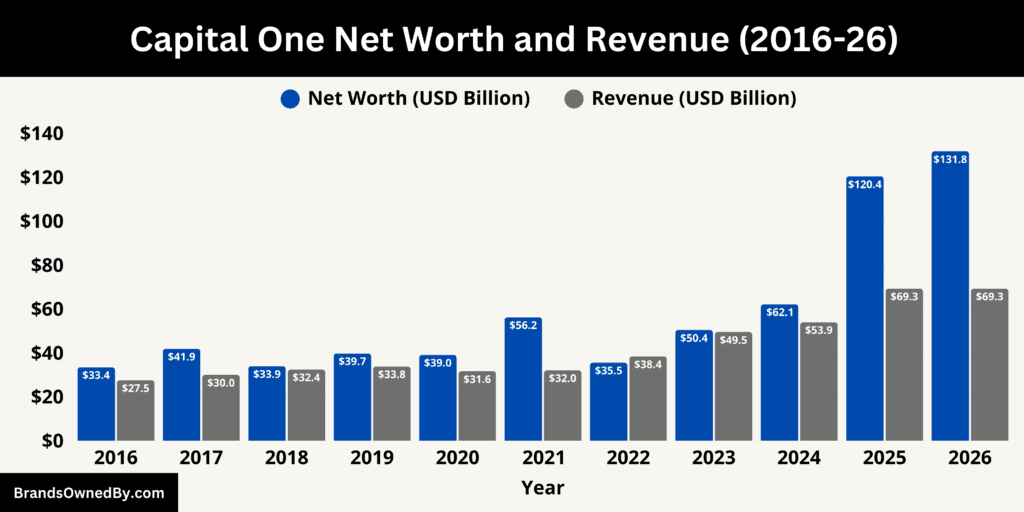

As of February 2026, Capital One Financial Corporation reports TTM revenue of $69.25 billion and an estimated market capitalization of $131.83 billion. Total assets exceed $470 billion. Total deposits are above $350 billion. The company operates one of the largest credit card loan portfolios in the United States. Revenue is driven primarily by interest income from consumer lending. Net worth reflects equity market valuation based on earnings power, credit risk exposure, and capital strength.

2026 Revenue

Capital One’s $69.25 billion trailing twelve-month revenue is composed of two primary streams:

Net interest income accounts for approximately $52–54 billion of total revenue. This represents earnings from credit card balances, auto loans, and commercial lending portfolios. Credit cards remain the dominant contributor within interest income due to higher yield spreads.

Non-interest income contributes approximately $15–17 billion. This includes interchange fees from card transactions, service charges, treasury management income, and other fee-based activities.

Segment contribution is concentrated as follows:

- Credit Card Segment: The largest revenue driver. It generates more than half of the total company revenue. Capital One is among the top U.S. card issuers by purchase volume and receivables.

- Consumer Banking: Generates revenue from deposit spreads, mortgage servicing, and retail lending. Digital banking under Capital One 360 continues to support deposit growth.

- Commercial Banking: Contributes through middle-market lending, commercial real estate, and specialty finance.

- Auto Finance: Produces interest income from dealership-originated and direct auto loans.

Loan portfolio composition heavily influences revenue performance. Higher average credit card balances and sustained consumer spending have supported interest income expansion in recent years.

Profitability and Balance Sheet Strength

Revenue alone does not determine financial strength. Capital One’s profitability depends on credit loss provisions and operating efficiency.

Provisions for credit losses fluctuate with delinquency and charge-off rates. Credit card charge-offs directly affect earnings due to the unsecured nature of the portfolio.

Capital One maintains regulatory capital ratios above required minimums under Federal Reserve supervision. Its Common Equity Tier 1 (CET1) ratio remains within strong compliance thresholds for large U.S. banks. Capital levels influence dividend policy and share repurchases, which in turn impact shareholder value.

2026 Net Worth

As of February 2026, Capital One’s estimated net worth stands at $131.83 billion.

Market capitalization is calculated as the share price multiplied by outstanding shares. This valuation reflects forward earnings expectations and risk-adjusted return assumptions.

Compared to diversified global banks such as JPMorgan Chase and Bank of America, Capital One trades at a valuation consistent with consumer-focused lenders. Its concentration in credit cards creates higher yield potential but also higher credit risk sensitivity.

Valuation is influenced by:

- Net interest margin trends

- Consumer delinquency rates

- Return on equity levels

- Federal Reserve interest rate policy

- Economic growth expectations.

Historical Revenue Growth (2016–2026)

Revenue increased from $27.52 billion in 2016 to $69.25 billion in 2026 TTM. This represents more than 2.5x growth over ten years.

Growth accelerated after 2022 due to:

- Higher benchmark interest rates expanding net interest margins

- Increased credit card receivables

- Expanded commercial banking exposure

- Strong consumer spending recovery.

The credit card segment remains structurally the highest-margin revenue contributor.

Revenue Forecast Through 2030

Projected revenue growth is driven by loan growth, deposit expansion, and margin dynamics. Based on current trajectory and moderate economic assumptions, forward estimates are:

- 2026 (Full Year Projection): $70–72 billion

- 2027: $74–76 billion assuming stable credit performance

- 2028: $78–81 billion supported by digital banking growth

- 2029: $83–86 billion with commercial portfolio expansion

- 2030: $88–92 billion assuming steady consumer demand and controlled credit losses.

These projections assume moderate economic growth and stable delinquency levels. A recession or sharp interest rate cuts would likely compress net interest income and reduce revenue growth.

Long-Term Net Worth Outlook

If revenue approaches $90 billion by 2030 and return on equity remains competitive, market capitalization could expand toward the $160–180 billion range under stable credit conditions.

However, valuation expansion depends heavily on credit quality stability and capital efficiency.

In summary, as of February 2026, Capital One generates $69.25 billion in annualized revenue and carries a market valuation of $131.83 billion. Its financial performance is primarily driven by credit card lending scale, interest rate environment, and disciplined risk management.

Companies Owned by Capital One

Capital One Financial Corporation operates through a structured network of national banks, regulated subsidiaries, financing entities, broker-dealers, servicing companies, and integrated acquisitions.

As of 2026, Capital One does not operate as a multi-brand conglomerate. However, it controls numerous legally distinct subsidiaries that handle credit issuance, deposits, securitization, auto lending, commercial banking, venture investments, and technology operations.

| Entity / Brand | Entity Type | Year Acquired / Formed | Primary Function | Strategic Importance |

|---|---|---|---|---|

| Capital One, National Association | National Bank Subsidiary | 1994 (chartered post spin-off) | Retail & commercial banking, deposits, business lending | Core deposit base; primary banking charter; funding engine |

| Capital One Bank (USA), National Association | National Bank Subsidiary | 1994 | Credit card issuing & receivables management | Largest revenue driver; unsecured lending platform |

| Discover Financial Services | Acquired Subsidiary | 2025 | Credit card issuing & payments network | Vertical integration; adds proprietary payments network |

| Discover Card | Consumer Brand | 1985 (acquired 2025) | Consumer credit card products | Expands prime customer base; strengthens card portfolio |

| Pulse (debit network) | Payments Network | 2005 (via Discover; acquired 2025) | Debit & ATM transaction processing | Diversifies into debit network revenue |

| Capital One 360 | Digital Banking Brand | 2012 (via ING Direct) | Online checking, savings, CDs | Drives low-cost deposit growth |

| Capital One Auto Finance | Lending Division | Internal | Auto loan origination & servicing | Secured lending diversification |

| Capital One Commercial Banking | Commercial Division | Internal expansion | Middle-market & corporate lending | Earnings diversification beyond consumer |

| Capital One Securities, Inc. | Broker-Dealer | Internal subsidiary | Capital markets & securitization support | Supports funding & institutional execution |

| TripleTree | Investment Banking Subsidiary | 2021 | Healthcare M&A advisory | Sector specialization & advisory revenue |

| KippsDeSanto & Co. | Investment Banking Subsidiary | 2022 | Aerospace & defense M&A advisory | Expands government-sector advisory presence |

| Capital One Equipment Finance | Commercial Lending Division | Internal | Equipment leasing & asset finance | Secured commercial lending expansion |

| Capital One Ventures | Venture Capital Arm | 2018 | Fintech & technology investments | Strategic innovation pipeline |

| Ocean Credit Card | UK Credit Brand | Operated via UK entity | Credit-building credit cards (UK) | International consumer expansion |

| Luma Credit Card | UK Credit Brand | Operated via UK entity | Credit-building credit cards (UK) | UK near-prime market positioning |

| Capital One Securitization Trusts | Financing Vehicles | Ongoing | Asset-backed securities issuance | Liquidity & balance sheet optimization |

| Capital One Cafés | Retail Banking Format | 2014 rollout | Hybrid banking/community locations | Customer engagement & brand presence |

Capital One, National Association

Capital One, N.A. is the company’s primary federally chartered bank and the core deposit-taking entity. It holds the majority of Capital One’s consumer and commercial deposits, services branch operations, and underpins retail and commercial bank products. This chartered bank is the principal vehicle for deposit accounts, business banking, treasury services, and many consumer loan products within the consolidated group.

Capital One Bank (USA), National Association

Capital One Bank (USA), N.A. is the group’s credit-card bank subsidiary that issues consumer and small-business credit cards and manages the card receivables book. It houses the card underwriting engines, credit servicing operations, collections, and related support functions that make the credit card business the single largest revenue engine in the Capital One group.

Capital One 360

Capital One 360 is Capital One’s digital retail banking brand, created after the acquisition and rebranding of ING Direct USA. It operates online checking, savings, high-yield accounts, CDs, and digital money management tools. The brand remains the primary online deposit franchise for customer acquisition and low-cost funding across the consolidated bank.

Capital One Auto Finance

Capital One Auto Finance is the company’s vehicle-lending platform. Operating through the bank subsidiaries, it originates indirect dealer loans and direct consumer auto loans, services auto receivables, and manages related dealer relationships and digital financing channels. The division is a major secured-lending arm within the group’s loan mix.

Capital One Commercial Banking

Capital One Commercial Banking is the group unit serving middle-market and corporate clients. It provides commercial and industrial lending, commercial real estate finance, treasury and payment services, and specialty finance (including healthcare and energy finance). The division operates as an integrated commercial business within Capital One, N.A.

Capital One Securities, Inc.

Capital One Securities, Inc. is the group’s broker-dealer and capital-markets subsidiary. It enables capital-markets execution, underwriting, and institutional sales activity that support corporate and commercial customers as well as internal securitization and funding programs.

Capital One Equipment Finance

Capital One Equipment Finance provides leasing and asset-based lending for equipment across transportation, construction, and industrial verticals. It operates within the commercial finance footprint to diversify secured lending beyond auto and real estate.

Capital One Ventures

Capital One Ventures is the corporate venture arm that makes strategic minority investments in fintech, data, cybersecurity, and cloud/AI companies. Investments are intended to accelerate product innovation and technology access for Capital One’s banking platforms and risk/analytical capabilities.

Capital One Labs / Technology & Data Platforms

Capital One operates internal technology, data science, cloud migration, and experimentation organizations often referred to collectively as Capital One Labs or the company’s tech engineering units. These legal and operational units support proprietary credit models, fraud detection, cloud-native banking infrastructure, and AI/data platforms used across subsidiaries.

Capital One Cafés

Capital One Cafés are branded retail locations that combine branch services with community space and in-person advisory. They are a customer-facing retail format operated directly by Capital One’s consumer banking organization to drive deposit acquisition and digital adoption.

Securitization Trusts and Funding Vehicles

Capital One sponsors and controls numerous asset-backed securitization trusts and financing entities that issue card- and auto-backed securities. These trusts are legally separate conduits used for funding and liquidity management but remain controlled for consolidation and risk management purposes.

TripleTree

TripleTree is an investment banking advisory platform focused on healthcare technology and services. Capital One announced and closed its acquisition of TripleTree (the agreement was announced in 2021 and subsequently closed). TripleTree operates within Capital One Commercial Bank’s capital markets capabilities and provides sector-specialist advisory services under the Capital One umbrella.

KippsDeSanto & Co.

KippsDeSanto & Co. is an M&A advisory and investment banking firm focused on aerospace & defense, government services, and enterprise technology. Capital One entered into an acquisition agreement for KippsDeSanto and the firm has operated as a Capital One subsidiary since that acquisition. The business provides deal advisory and industry expertise that complements Capital One’s corporate and government client coverage.

Discover Financial Services and Discover Card

Capital One completed the acquisition of Discover Financial Services in 2025, bringing the Discover payments network and Discover Card brand into the Capital One family. Post-close, Discover’s issuer, network, and consumer products operate as a major group business within Capital One, significantly expanding the company’s card base, payments infrastructure, and merchant network capabilities.

Ocean

Ocean (trading as Ocean Finance / Ocean Credit Card) refers to consumer credit card programs and branded card products marketed in the UK, where Capital One is the issuing bank. In these arrangements, Ocean-branded cards are issued by Capital One as the regulated issuer; the Ocean name functions as a marketing partner/brand in the UK market rather than as an independent non-bank corporate group outside Capital One’s control.

Luma

“Luma” appears in Capital One’s UK product footprint as a branded quick-check or consumer interface (for example, a Capital One Luma QuickCheck site used in some market processes). This should not be conflated with independent companies named “Luma Financial Technologies” or “Luma AI.”

In Capital One’s case, Luma references are branded product/portal names and digital touchpoints that operate under Capital One’s regulated entities in markets where the company issues consumer credit or loan-related products.

Internal Advisory and Specialty Units

Capital One operates internal teams and units that manage payment rails, merchant acquiring relationships, and card-processing services. These groups include legacy product teams and platforms that operate under the Capital One legal entities rather than as independent external brands.

Conclusion

Capital One is a publicly traded financial institution with dispersed ownership across institutional investors, funds, and individual shareholders. There is no majority owner or parent company controlling the business. Instead, governance flows through shareholder voting, board oversight, and executive leadership.

When examining who owns Capital One, the answer reflects a modern bank holding company structure. Ownership is broad, while operational control is centralized within management and regulated banking subsidiaries. The company’s structure, acquisitions, and integrated divisions demonstrate how large U.S. banks operate today — publicly held, institutionally influenced, and professionally managed.

FAQs

Who bought Capital One?

No company has bought Capital One Financial Corporation. It is an independent, publicly traded bank holding company listed on the New York Stock Exchange. Its shares are owned by institutional and retail investors.

Is Capital One JP Morgan?

No. Capital One Financial Corporation and JPMorgan Chase are separate, competing financial institutions. They operate independently with different management, boards, and shareholders.

Who is the founder of Capital One?

Richard D. Fairbank and Nigel Morris founded Capital One in 1994 after it was spun off from Signet Financial.

Which bank is behind Capital One?

Capital One operates through its own national bank subsidiaries, primarily Capital One, N.A. and Capital One Bank (USA), N.A. It is not backed by another bank. It is a standalone bank holding company regulated by U.S. federal authorities.

Does HSBC own Capital One?

No. HSBC does not own Capital One. The two institutions are separate global banking organizations.

Does Warren Buffett own Capital One?

Warren Buffett does not personally own Capital One. However, his company Berkshire Hathaway has previously held shares in various U.S. banks. Any ownership would be through publicly traded stock holdings, not private control.

Who did Capital One bank merge with?

Capital One has completed several major acquisitions rather than mergers of equals. Notable acquisitions include Hibernia National Bank in 2005, North Fork Bancorporation in 2006, and ING Direct USA in 2012. In 2025, it acquired Discover Financial Services.

Is Capital One owned by Chase?

No. JPMorgan Chase does not own Capital One. They are competitors in credit cards and banking.

Who is the CEO of Capital One?

As of 2026, Richard D. Fairbank serves as Chairman and Chief Executive Officer of Capital One.

Is Capital One owned by Citibank?

No. Citigroup (Citibank’s parent company) does not own Capital One. They are separate publicly traded banks.

Are Chase and Capital One the same?

No. Capital One Financial Corporation and JPMorgan Chase are distinct companies with separate ownership and management.

Who owns Capital One in the United States?

Capital One is owned by public shareholders in the United States and globally. The largest shareholders as of 2026 are institutional investors such as The Vanguard Group and BlackRock. No single shareholder controls the company.